Table of Contents

- Paytm: Journey so far

- What is Paytm’s Moat?

- Industry Overview

- Cashless Payments & Mobile transactions

- Indian Digital Lending market

- Insurance Tech market

- Competitive Landscape

- Market Share

- Paytm Revenue Model

- 1/ Payment Services

- 2/ Financial Services:

- 3/ Marketing Services:

- Cost Levers for Paytm

- 1. Marketing Expenses:

- 2. Employee Expenses:

- 3. Cloud Infrastructure Costs:

- Key Metrics to Track for Paytm

- 1/ Merchant Payments Volume (GMV):

- 2/ Average Monthly Transacting Users (MTU):

- 3/ Loan Disbursements:

- Future Opportunities for Paytm

- 1/ Mobile Distribution of Credit:

- 2/ Emerging Payment Technologies:

- 3/ Expansion in Financial Services:

- Business Challenges for Paytm

- 1/ Losing Market Share

- 2/ Inability to Provide Services via PPL

- 3/ Compliance and Regulatory Issues

- 4/ Operational Disruption

Do not index

CTA Headline

CTA Description

CTA Button Link

Paytm: Journey so far

22 year old Vijay Shekhar Sharma started One97 Communications in 2000 — a website which offered news, cricket scores, ringtones, jokes and exam results. 10 years later, it became the parent company of one of India’s largest financial and digital payment services company we all know as Paytm.

A vision for a cashless economy and robust tech integration has helped Paytm hold an impressive market position in the industry.

Today, Paytm is synonymous with digital payments in India, offering everything from simple mobile recharges to personal loans—all at the tap of a button.

With over ~8 million monthly transacting users and 4 lakh+ merchant partners, Paytm has mastered user acquisition and retention, with a wide scope of diverse services to upsell and cross-sell.

If you want to understand the Indian financial landscape and the growing demand for cashless and paperless transactions, you’ve come to the right place. In this blog, we discuss how Paytm is navigating the ebbs and flows of the industry and dig deeper into its revenue generating services.

If you are interested to uncover business models of internet-first companies, you can check out Airbnb Business Model & other blogs here.

What is Paytm’s Moat?

Paytm's journey to becoming a household name in India took a significant leap forward during the 2016 demonetization.

When the government imposed demonetization, the nation was thrust into a cash crunch.

Paytm — a growing player in the digital payments space, seized the opportunity. The platform became a go-to alternative for millions, offering a convenient way to conduct transactions without cash.

By 2017, Paytm had garnered over 280 million users, and its acceptance spanned even the smallest villages in India. This massive adoption solidified Paytm’s reputation as a trusted and reliable platform. Today, both merchants and consumers continue to prefer Paytm for several reasons:

- Paytm’s interface is designed to be intuitive and user-friendly, making it accessible to people across all digital literacy levels. Whether it's paying bills or receiving payments, the process is quick and hassle-free.

Paytm provides a range of services within its app, from digital payments to insurance, all under one app. This all-in-one approach ensures users have everything they need in a single platform, enhancing convenience.

- Paytm’s early and widespread adoption, particularly post-demonetization, has established it as a trusted platform across India. Its presence in both urban and rural areas has made it a preferred choice for many.

- Paytm continues to introduce new features, like the Soundbox, making it easier for merchants to manage transactions, even in noisy environments.

- Paytm’s commitment to evolving and expanding its services ensures that it remains relevant and continues to meet the changing needs of its users.

By the way, the depth you see here is just a feeler of the depth we teach at GrowthX 💫

GrowthX is an invite-only club of over 3000 members who are product, marketing, and business leaders, and founders from top internet-first companies like Google, Canva, CRED, Stripe, Netflix, and more 💎

We teach our members how to scale revenues via frameworks that can be applied starting next Monday morning. The GrowthX Membership is built on 3 core pillars:

1. Learning experience: Where you learn the science of revenue-led growth with frameworks actionable the next Monday morning.

2. Curated community: Where you access a safe space for you to soundboard anything that is stressing you at work.

3. Career outcomes: Over 35% of members are founders & are able to hire growth teams to scale revenue for their companies while operators are able to get into breakout leadership roles.

Explore GrowthX Membership 🏆

Industry Overview

India is on the cusp of becoming a $7 trillion economy, driven by an ambitious vision of digitization across its financial and payment sectors.

- The government has strategically focused on reviving the nation's growth potential by implementing policies that bolster the financial sector, simplify business landscapes, and significantly upgrade physical and digital infrastructure.

- The development of digital infrastructure has been a game-changer, enabling the creation of digital identities, broadening access to finance, and reducing transaction costs.

- Fintech companies, powered by initiatives like India Stack, are at the forefront of this revolution, driving financial inclusion even in Tier 3 and beyond markets.

As India continues to digitalize, these fintech innovations will be key drivers of growth, positioning the country as a global leader in the digital economy.

.png?id=2a43578d-c3f0-81e2-8f2e-cc921bc09928)

Cashless Payments & Mobile transactions

India’s digital payments landscape has transformed rapidly, becoming a key driver of economic growth.

The government’s digitization initiatives have paved the way for greater financial inclusion, making digital payments a cornerstone of India’s financial ecosystem.

Unified Payments Interface (UPI), introduced in 2016, has revolutionized how Indians transact, facilitating easy and instant fund transfers across bank accounts.

UPI’s success is evident in its widespread adoption, with Indians using UPI apps for ~80% of transactions across grocery, food delivery, and travel sectors.

The surge in Person to Merchant (P2M) payments, particularly through QR codes, has further boosted digital transactions, especially in the retail sector.

Currently, 35% of Indian households conduct digital transactions, a figure expected to reach 50% by 2026.

With digital payments becoming increasingly mainstream, fintech companies are innovating to meet the growing demand, and Paytm is at the forefront of this transformation.

.png?id=2a43578d-c3f0-8113-9932-ce14a688bb40)

Indian Digital Lending market

The digital lending market is projected to grow at a CAGR of 33%, reaching $515 billion by 2030.

The digital lending market in India is experiencing exponential growth, driven by the rise of Buy Now Pay Later (BNPL) services.

- BNPL has become a mainstream payment option, particularly favored by Gen Z and millennials, who are now indulging in high-ticket purchases with the convenience of EMIs.

- E-marketplaces like Amazon are also playing a crucial role in shaping consumer behavior by integrating lending products at the point of purchase.

- This trend is not limited to B2C; BNPL is also gaining traction in the B2B space, offering businesses flexible payment solutions.

The availability of large customer data sets has made market entry easier for digital lenders, allowing them to offer loans with better margins than other fintech models.

Insurance Tech market

The Insurance Tech market in India is expected to hit $88 billion by 2028, reflecting the growing demand for digital insurance solutions.

Companies in this space are working hard to create more personalized and flexible insurance products, catering to the diverse needs of consumers in an increasingly digital world.

The industry has evolved significantly, expanding beyond a one-size-fits-all approach into areas such as underwriting, bite-sized or specialty insurance, and health insurance via analytics providers for better decision-making.

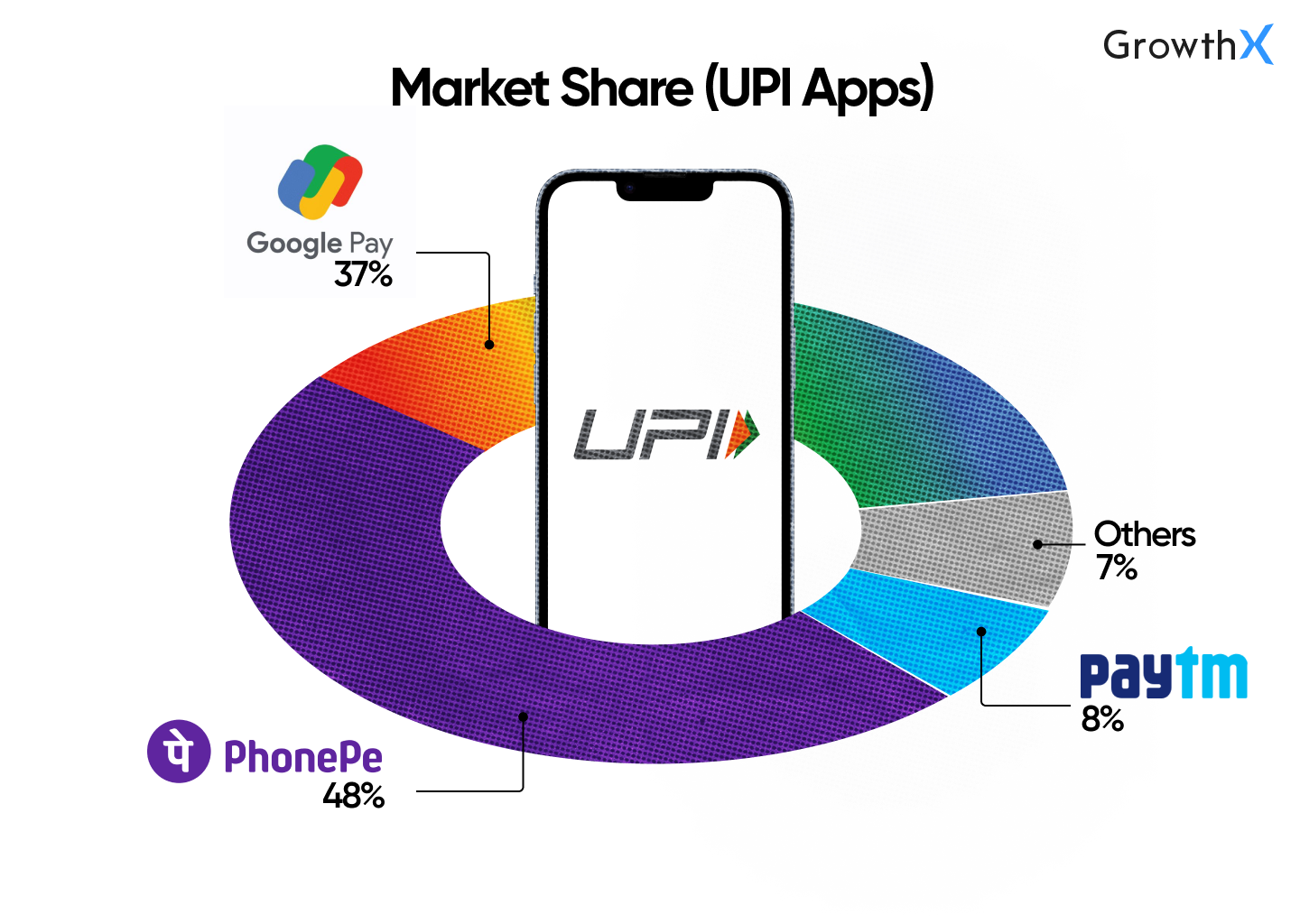

Competitive Landscape

When we talk about the competitors in the payments landscape we need to consider one thing —

Since all UPI apps operate on the same underlying infrastructure provided by the National Payments Corporation of India (NPCI), users can switch between apps without changing their UPI ID.

The UPI ID is linked to the user's bank account, not the app, so users can simply log in to a new app using their existing UPI credentials.

Switching to a different UPI app involves minimal steps —

Users typically need to download the app → authenticate via their registered mobile number (linked to their bank account)→ set up a new app-specific PIN if required.

Since the UPI ID remains the same, all linked bank accounts are automatically recognized, making the transition smooth.

This is a boon for the customer who is spoilt with choices but a bane for these fintech companies since the CAC goes down the drain.

With that in mind, let's take a look at players in the digital payments ecosystem who are giving Paytm a run for its money. This table shows various points of parity to understand the use case and popularity of each brand 👇🏻

Metric | Paytm | PhonePe | Google Pay | CRED | Amazon Pay | FamPay |

Use Case | A super app offering payments, financial services, and commerce | A digital payments platform with a strong UPI presence | A UPI-based payments app with a focus on simplicity | A platform rewarding users for paying credit card bills | A digital wallet and payments service linked to Amazon shopping | A payments app designed for teenagers |

Launched In | 2010 | 2015 | 2017 | 2018 | 2016 | 2019 |

MTU (Monthly Active Users) | 90 million+ | 480 million+ | 150 million+ | 12 million+ | 50 million+ | 2 million+ |

Services Offered | Payments, banking, insurance, wealth management, e-commerce | UPI payments, mobile recharges, bill payments, insurance | UPI payments, bill payments, peer-to-peer transfers, loans | UPI payments, Credit card payments, rewards, personal loans | UPI payments, mobile recharges, bill payments, Amazon services | UPI payments, card payments, rewards, saving goals |

Transaction Volume (2023-24) | ₹123 crores | ₹650 crores | ₹506 crores | ₹13 crores | ₹6 crores | ₹4 crores |

USP | Extensive financial services and commerce ecosystem | High UPI adoption and integration | Simplified UPI transactions with a Google ecosystem | Credit score improvement and exclusive rewards | Seamless integration with Amazon's ecosystem | Tailored for teenagers with a focus on financial education |

Market Share

To cut through the noise, a strong SEO strategy will help you outshine your competitors.

If you want to learn more, we have something special for you 💫

FREE access to SEO Foundations by GrowthX.

Whether you're looking to refine your strategy or start from scratch, this no-fluff, insight-packed resource is designed with input from experts at top companies like Flipkart, Zepto, and more.

Click here to access now 💎

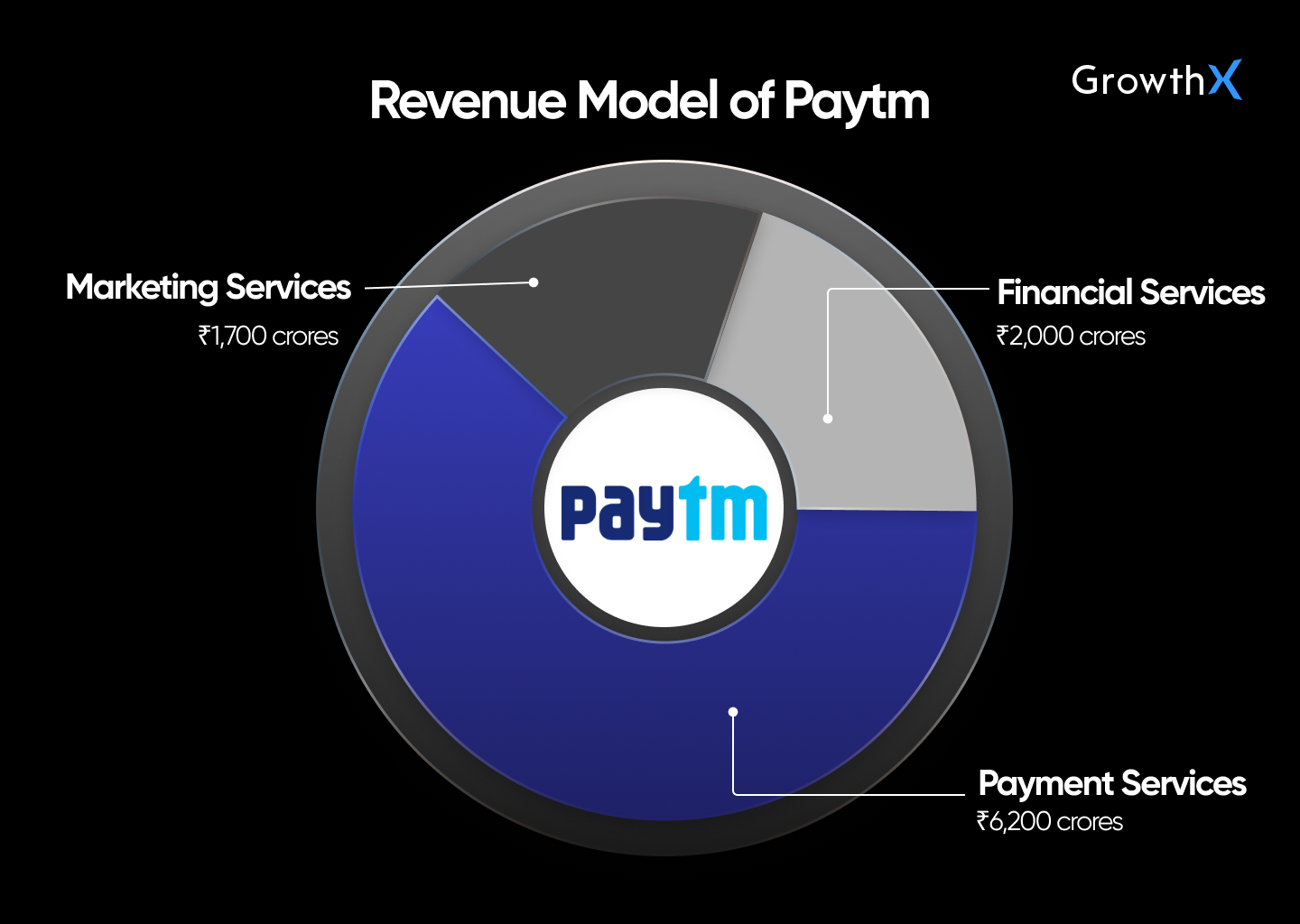

Paytm Revenue Model

Paytm has evolved into a powerhouse in India’s digital economy, with a revenue model that leverages its payments platform to acquire customers and then cross-sell and upsell financial services.

By acting as a two-way marketplace for both customers and merchants, Paytm has created a diversified revenue engine that sustains its growth and influence.

1/ Payment Services

a. Payment Solutions for Customers

Paytm’s journey begins with its robust payment services that cater to individual customers. These include:

- Peer-to-Peer (P2P) Transactions

- UPI & UPI Lite

- Credit Cards

- Utility Bill Payments

- Recharges

Every time a customer uses Paytm for these transactions, the company earns a small fee, particularly from credit card payments and government incentives related to UPI transactions.

Following are charges levied by Paytm for various payment sources:

Online Payments MDR (Standard Plan)

Payment Source | Merchant Discount Rate (MDR) |

UPI | 0% |

Paytm Bank Wallet | 1.99% |

Paytm Postpaid | 1.99% |

Rupay Debit Cards | 0% |

Debit Cards (Visa, Mastercard, Maestro)

Up to ₹2,000 | 0.40% |

Over ₹2,000 | 0.90% |

Credit Cards (Visa, Mastercard, RuPay) | 1.99% |

Other Cards (Amex, Diners, Prepaid, Corporate & International Cards) | 2.99% |

Netbanking | 1.99% |

EMI (Debit Cards, Credit Cards or Cardless EMI) | 2.99% |

b. Payment Solutions for Merchants

Merchants form the backbone of Paytm’s ecosystem, and the company offers several payment solutions to meet their needs:

- QR Codes

- Card Machines

- Payment Gateways

- POS (Point of Sale) Machines

Merchants use these devices not only for accepting payments but also for fraud prevention and reconciliation services. With support for 11 languages, including regional languages, Paytm’s devices have rapidly been adopted across the country, empowering small and micro-businesses.

Revenue Streams for Payment Services:

- Paytm earns revenues from processing all types of payments, including incentives from the government for UPI transactions and MDR (Merchant Discount Rate) on payments made via Rupay Credit Card on UPI.

- Subscription revenues are significant—from merchants using Paytm’s payment devices like Soundboxes and EDC machines. The number of deployed payment devices rose from 68 lakh in 2023 to 107 lakh in 2024, with 1 crore+ merchants currently subscribed.

- The Paytm Soundbox starts at ₹999 and merchants pay ₹99 per month.

These are the rates levied by Paytm for merchants using their app/devices to process payments.

In-Store Payments MDR (Standard Plan)

Payment Source | Use Case | Small Merchant | Big Merchant |

UPI | - | 0% | 0% |

Paytm Bank Wallet/Paytm Voucher/Loyalty | - | 1.25% | 1.25% |

Paytm Postpaid | - | 1.50% | 1.50% |

Rupay Debit Cards | - | 0% | 0% |

Debit Cards (Visa, Mastercard, Maestro) | - | 0.40% | 0.90% |

Credit Cards (Visa, Mastercard, RuPay) | Grocery/Kirana Categories | 1.40% | 1.40% |

ㅤ | Tolls/Utilities/Education Categories | 1.20% | 1.20% |

ㅤ | Other Categories | 1.99% | 1.99% |

American Express | Retail (except Electronics) | 2.60% | 2.60% |

ㅤ | Hotels, Car Rentals | 3.99% | 3.99% |

ㅤ | Education, Electronics, Utilities | 1.99% | 1.99% |

ㅤ | Healthcare & Pharmacy | 2.20% | 2.20% |

Corporate/Commercial Cards (Credit Card) | - | 2.75% | 2.75% |

International Card | - | 3.50% | 3.50% |

Diners/UCB/Union Pay Card | - | 2.90% | 2.90% |

Prepaid Card | - | 2.75% | 2.75% |

Corporate/Commercial Card (Debit Card) | - | 0.40% | 0.90% |

2/ Financial Services:

a. Lending: Personal and Merchant Loans

Paytm’s financial services extend beyond payments to include lending, facilitated through partnerships with banks:

- Personal Loans

- Merchant Loans

In 2024, Paytm’s lending partners disbursed loans totaling ₹52,390 crore, a 48% increase from the previous year to over 2 Crore whitelist users.

- A sourcing fee from the financial institution partners, which is earned at loan disbursal based on the loan amount percentage.

- A collection fee from those financial institution partners based on the loan amount percentage through Paytm’s collection services.

b. Wealth Management: Paytm Money

Paytm is also expanding its presence in wealth management by distributing mutual funds, capitalizing on the growing participation of retail investors in the equity markets.

Paytm earns consumer fees, such as an upfront account opening fee, transaction fees depending on transaction type and volumes, and an annual subscription fee.

To learn more about India’s growing investor class and their faith in mutual funds, check out this Inner Circle Episode with Vishal Jain, CEO of Zerodha Fund House where he shares his journey and how he pioneered India’s First ETF in 2001 and how he leads Zerodha Fund House, which has amassed an AUM of 500 Crores in just three months!

c. Insurance Broking: Paytm Insurance

Paytm's insurance broking arm is gaining early momentum, demonstrating a promising product-market fit.

The company is focusing on both embedded insurance solutions, which are seamlessly integrated into its existing offerings, as well as merchant insurance products tailored specifically for businesses.

This dual approach positions Paytm to capitalize on the growing demand for insurance solutions among both consumers and merchants, further diversifying its revenue streams in the financial services sector.

3/ Marketing Services:

Paytm generates revenue through various consumer services, including:

- Movie Ticketing

- Gift Vouchers

- Advertising

- Loyalty Points

b. Co-branded Credit Cards

Paytm's co-branded credit cards, launched with SBI Card, HDFC Bank, and Kotak Bank, are a key revenue source. By March 2024, 1.2 million of these cards were activated, generating revenue from both activation fees and a portion of transaction fees.

But what is the hype around co-branded credit cards?

We sat down with Vikash Singh, Director Of Growth @Flipkart and an OIR at GrowthX where he talks about GTM strategies and highlights insights about the co-branded credit card industry. Watch him on GrowthX Insider here 👇🏻

Revenue Streams for Marketing Services:

- Transaction fees are charged to merchants and convenience fees to customers, typically as a percentage of the transaction value, covering services like travel, entertainment, and deals.

- Paytm also earns subscription and volume-based fees for cloud and software solutions provided to merchants.

- Advertising partners contribute to revenue based on the scale and type of campaigns run on Paytm’s platform.

Paytm’s revenue model is a well-oiled machine, driven by a diverse array of income streams. Starting with payments, the company successfully cross-sells financial and marketing services, ensuring sustained growth. As Paytm continues to innovate and expand its offerings, its revenue model remains a key pillar supporting its leadership in the fintech space.

Cost Levers for Paytm

Effective cost management is critical for Paytm's continued growth and profitability. The company has implemented several strategies to optimize its expenses across different domains:

1. Marketing Expenses:

Marketing expenses include costs for advertising, promotions, and customer acquisition. Paytm optimizes these by focusing on targeted, data-driven campaigns and leveraging digital channels for better efficiency.

2. Employee Expenses:

Employee expenses cover salaries, benefits, and related costs. Paytm is investing in key areas like technology and sales while optimizing by automating processes and streamlining non-core functions.

3. Cloud Infrastructure Costs:

These costs include software, cloud services, and data centers. Paytm is reducing them by using cost management tools, renegotiating contracts, and improving infrastructure efficiency.

By the way, the depth you see here is just a feeler of the depth we teach at GrowthX 💫

GrowthX is an invite-only club of over 3000 members who are product, marketing, and business leaders, and founders from top internet-first companies like Google, Canva, CRED, Stripe, Netflix, and more 💎

We teach our members how to scale revenues via frameworks that can be applied starting next Monday morning. The GrowthX Membership is built on 3 core pillars:

1. Learning experience: Where you learn the science of revenue-led growth with frameworks actionable the next Monday morning.

2. Curated community: Where you access a safe space for you to soundboard anything that is stressing you at work.

3. Career outcomes: Over 35% of members are founders & are able to hire growth teams to scale revenue for their companies while operators are able to get into breakout leadership roles.

Explore GrowthX Membership 🏆

Key Metrics to Track for Paytm

Monitoring key performance indicators (KPIs) is crucial for understanding Paytm's business health and growth trajectory. Some of the vital metrics to track include:

1/ Merchant Payments Volume (GMV):

The Gross Merchandise Value (GMV) processed through Paytm’s platform is a core metric that reflects the scale of merchant transactions. A growing GMV indicates increased merchant adoption and transaction volume, both of which contribute to Paytm’s revenue growth.

2/ Average Monthly Transacting Users (MTU):

Tracking the average number of monthly transacting users is essential to gauge user engagement and the effectiveness of Paytm's customer retention strategies. Higher MTU figures suggest strong user activity and loyalty on the platform.

3/ Loan Disbursements:

Paytm’s success in financial services can be measured by the value and number of loans disbursed. In FY2024, loan disbursements reached ₹52,390 crore, showcasing significant growth in this segment. Monitoring both the total value and the number of loans distributed will provide insights into Paytm's lending business’s performance and scalability.

Future Opportunities for Paytm

As Paytm continues to innovate and expand, several emerging trends and growth vectors present significant opportunities:

1/ Mobile Distribution of Credit:

India’s massive and scalable credit market offers a profitable growth opportunity for Paytm. Leveraging its ecosystem, Paytm is well-positioned to address multiple large and fast-growing market segments, driving substantial revenue from mobile credit distribution.

2/ Emerging Payment Technologies:

Innovations such as e-Rupi, wearable payment devices, voice payments, and biometric payments are poised to enhance customer experience and increase digital spending. Retail e-Rupi has already seen impressive adoption, with approximately 800K transactions within two months of its launch. The Indian wearable market, valued at ₹1.1 lakh crore in FY22, is expected to reach ₹1.4 lakh crore by FY 2030, presenting a vast opportunity for Paytm to capitalize on these trends.

3/ Expansion in Financial Services:

Paytm’s early momentum in insurance, particularly in embedded and merchant insurance products, highlights the potential for further growth in financial services. Additionally, the expansion of mutual funds distribution and other wealth management offerings positions Paytm to capture a larger share of the financial services market.

Business Challenges for Paytm

1/ Losing Market Share

With a plethora of options in the digital payments sphere, customers are switching to competitors, resulting in a significant loss of market share, especially in digital payments and banking.

2/ Inability to Provide Services via PPL

The cessation of services like deposits, credit transactions, and FASTag recharges via Paytm Payments Bank has lead to decreased user engagement and loss of revenue from these transactions.

3/ Compliance and Regulatory Issues

Persistent compliance issues, such as improper account openings, have already led to severe actions from the Reserve Bank of India (RBI). Ongoing investigations could further strain operations, increasing operational costs and legal risks.

Continuous regulatory breaches may tarnish Paytm's brand, making it harder to gain customer trust and potentially affecting its valuation.

4/ Operational Disruption

Handling the fallout from service disruptions will put pressure on customer support operations, increasing costs and potentially leading to dissatisfaction if not managed effectively.

These challenges underscore the need for Paytm to swiftly address compliance issues, communicate effectively with stakeholders, and rebuild trust to mitigate long-term impacts on its business.