Table of Contents

- How was CRED founded? ✨

- Journey 💫

- CRED’s MOAT (Competitive Advantage) 💪🏻

- What problem does CRED solve? 🤔

- Market Overview 🏦

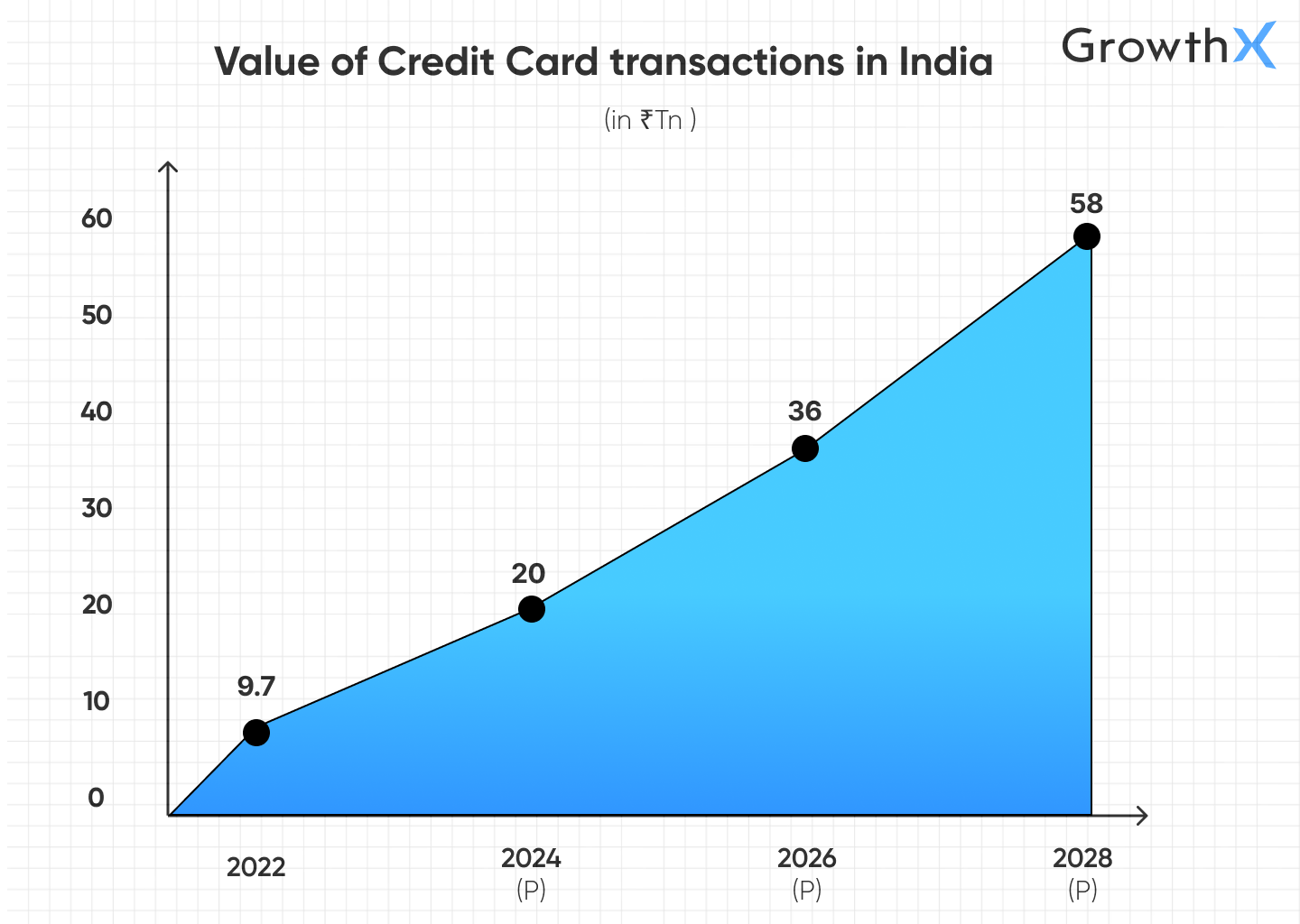

- Credit Cards

- Digital Lending

- Digital Payments

- Insurance

- Market Trends

- Competitive Landscape 🥊

- CRED

- 2. CRED Cash

- 3. Others

- Market Share

- How does CRED make money? 💰

- 1. Finance Sub-Products

- 2. Lifestyle Sub-Products

- Cost Levers 💸

- Market Opportunity

- Challenges

Do not index

CTA Headline

CTA Description

CTA Button Link

How was CRED founded? ✨

CRED was born from a simple observation: India’s credit system punished more than it rewarded.

Miss a payment? You’d face late fees, higher interest rates, and a damaged credit score. But where were the rewards for those who managed their finances well? 😤

This is where Kunal Shah saw an opportunity to flip the script. 💫

What if there was a platform that not only reminded people to pay their bills on time but also rewarded them for doing so? In 2018, CRED was launched to do exactly that—creating an exclusive club that recognises and rewards good financial behaviour.

Before CRED, Shah had already built and sold two successful startups: PaisaBack and FreeCharge. His experience laid the groundwork for CRED, a platform designed to address key pain points for credit card users.

If you are interested in uncovering the business models of other internet-first companies, you can check out Swiggy Business Model & other blogs here.

Journey 💫

With backing from top investors like Sequoia Capital and DST Global, CRED offered rewards like cashback, discounts, and even free flight tickets to incentivise timely bill payments and improve credit scores.

CRED quickly gained traction, becoming a unicorn within three years. By 2021, it had onboarded over 5.9 million users and was processing 20% of all credit card bill payments in India.

Fast forward to 2022, CRED was valued at $6.4B!!

Today, with ₹1,484 crore (FY23) revenue and 13 million MAUs, CRED has evolved into more than just a fintech app—it's a lifestyle brand serving a high-trust community with unique services and experiences.

CRED’s MOAT (Competitive Advantage) 💪🏻

- Exclusivity & Brand Positioning 🏅

Instead of targeting the masses, CRED focused on India’s top 25 million households—financially savvy and affluent individuals who value responsible credit management.

This approach has allowed CRED to build a high-value community that’s attractive not only to users but also to brands eager to reach this premium audience.

While most finance apps are functional but forgettable, CRED stands out as a cool, aspirational brand that people talk about. It's not just about paying bills; it's about being part of an exclusive club that rewards good financial behaviour.

Unlike giants like Amazon and Paytm, CRED has carved out a unique niche where it’s the go-to name for rewarding credit card payments, creating a powerful brand moat that’s hard to replicate.

Speaking of brand positioning—there’s something even bigger that can set you apart: Founder Branding.

And when it comes to this, Kunal Shah knows his stuff.

Building a personal brand isn’t just a buzzword—it’s your golden ticket to hiring top talent, securing funding, and attracting customers.

If you're an early-stage founder or already in the pre-seed to Series A phase, we have something special for you!

It’s the FREE Founder Branding Foundation by GrowthX!

This guide will help you in making great first impressions online, maintain consistency across different touch points related to hiring, come up with a solid umbrella thought for your content and many more!!

- Trust & Selective User Base 🫶🏻

CRED’s trust factor is deeply tied to its selective user base.

By focusing on top CEOs, leaders, and affluent celebrities, CRED ensures it delivers exactly what these high-value users expect:

→ Security

→ Seamless experiences, and

→ Reliability.

When you concentrate on a smaller, more affluent group, you can better understand and cater to their needs, creating a deeply personalised and trustworthy experience that solves for two things:

1. This selective user base is inherently monetisable. These users have the means and willingness to engage with premium services, allowing CRED to scale effectively without spreading itself too thin.

2. This focus prevents the brand dilution that often occurs when companies try to be everything for everyone. Instead, CRED has built a strong, loyal customer base that deeply trusts the platform, making this trust a significant moat against competitors.

By the way, the depth you see here is just a feeler of the depth we teach at GrowthX 💫

GrowthX is an invite-only club of over 3000 members who are product, marketing, and business leaders, and founders from top internet-first companies like Google, Canva, CRED, Stripe, Netflix, and more 💎

We teach our members how to scale revenues via frameworks that can be applied starting next Monday morning. The GrowthX Membership is built on 3 core pillars:

1. Learning experience: Where you learn the science of revenue-led growth with frameworks actionable the next Monday morning.

2. Curated community: Where you access a safe space for you to soundboard anything that is stressing you at work.

3. Career outcomes: Over 35% of members are founders & are able to hire growth teams to scale revenue for their companies while operators are able to get into breakout leadership roles.

Explore GrowthX Membership 🏆

What problem does CRED solve? 🤔

Paying credit card bills through traditional banking portals is a frustrating experience due to their:

- Clunky, unresponsive interfaces

- Complex workflows, and

- Frequent transaction failures

Managing multiple cards with different due dates adds to the stress, often leading to missed payments, hidden charges, and tedious manual tracking of expenses. Users also struggle to keep up with changing offers and rewards, missing out on potential savings and benefits.

→ CRED’s solution 💡

CRED simplifies credit card management by centralising all your cards in one app. It offers:

1. Seamless Payments: Pay bills in just a few taps using UPI and other methods.

2. CRED Protect: Detect hidden charges, get reminders, and access spend insights across all cards.

3. Offer Optimisation: Track and optimise credit card offers with a single click.

Beyond bill payments, CRED enhances your experience with

- Exclusive Rewards: Earn CRED Coins for timely payments and redeem them for luxury products, vacations, and more.

- Financial Access: Get instant personal loans with CRED Cash and earn high returns with CRED Mint.

- Credit Score Tracking: Members get to track their credit score without having to visit third-party websites and avoid getting spammed by calls from financial institutions that sell loans and credit cards.

Market Overview 🏦

The Indian fintech industry is booming, estimated to hit approximately ₹9.13 lakh crore ($110 billion) in 2024 and projected to soar to roughly ₹35 lakh crore ($420 billion) by 2029.

CRED, with almost 90% of its revenue rooted in fintech (coming from CRED Cash, utility bill payments space, and insurance services), is right in the thick of this growth.

Let’s break down the key areas CRED is playing in 👇

Credit Cards

India ranks 8th globally with approximately 120 million active credit cards

By FY28-29, the number of credit cards is expected to roughly double, reaching 200 million, with a CAGR of 15%

Credit card transactions are surging too, transaction volumes have grown by 22%, while transaction values have surged by 28% 📈

The average cardholder spends ₹15.4K monthly across three transactions, showcasing how credit cards are becoming a daily tool for many.

But what is fuelling this growth? (Click on this to find out!)

- Credit Culture Shift: Credit is becoming more acceptable, even in regions where it was previously avoided. Both banks and consumers are embracing this change, fuelling credit card growth.

- Economic Momentum: India’s robust 7% GDP growth is boosting incomes across the board, making credit more accessible and appealing to a broader demographic.

- Personalised Offerings: Companies are rolling out credit cards tailored to specific consumer behaviours. For example, the Amazon Pay ICICI Credit Card is designed to match the spending patterns of frequent Amazon shoppers.

- Virtual Cards: The rise of virtual cards is making credit more accessible. Users can now add family members to their accounts with virtual cards, extending benefits without needing additional physical cards.

- Contactless Payments: With Near-field communication, which is a form of technology that enables communication between two devices, and Point of Sale machines that allow payments under ₹2,000 without swiping, contactless payments are speeding up transactions and improving customer experiences.

- RuPay's Growth: The government’s push for RuPay credit cards through public sector banks and the integration of UPI with RuPay cards is driving significant adoption, paving the way for further growth in credit card usage.

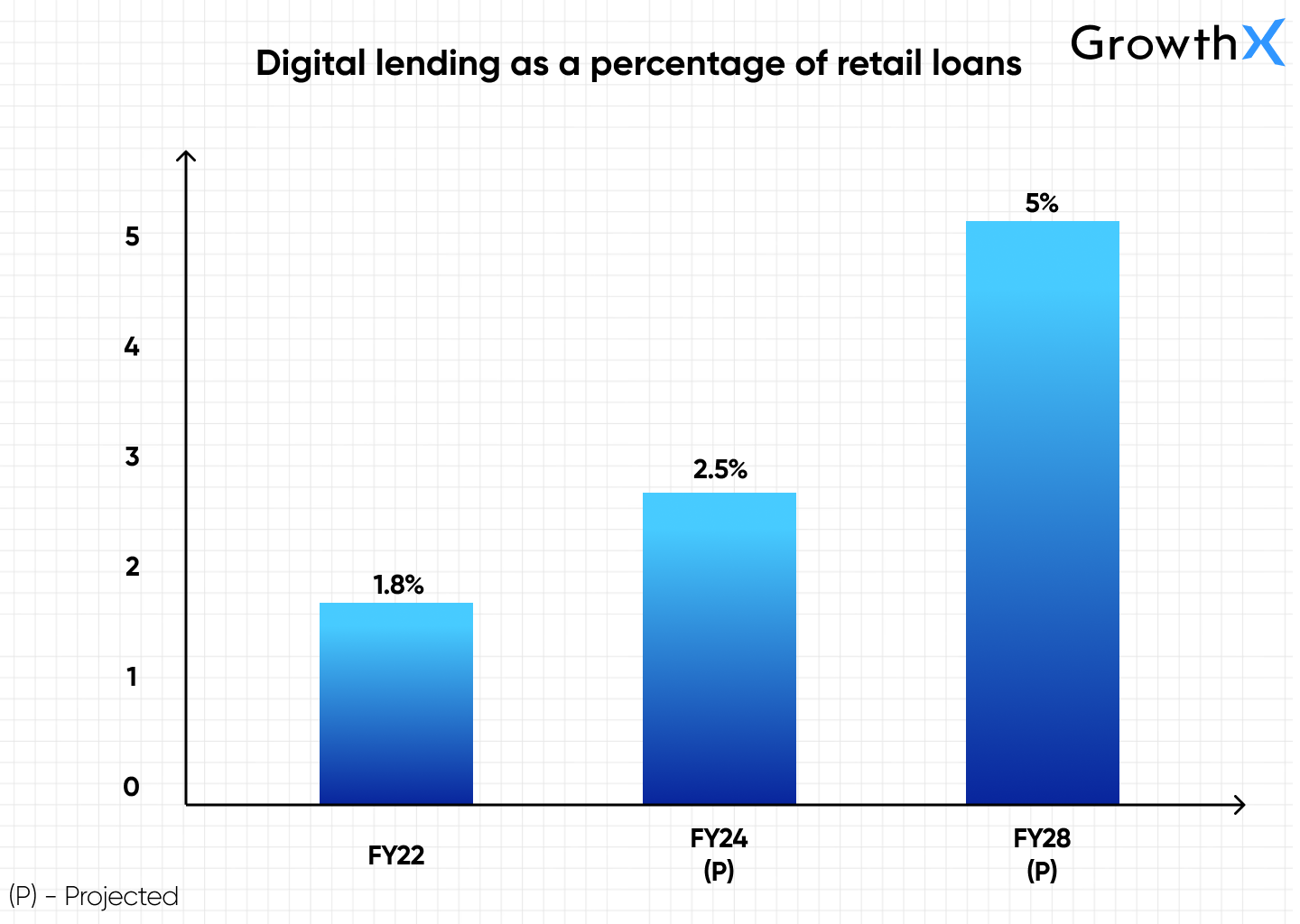

Digital Lending

Digital Lending market is set to surpass roughly ₹60 lakh crore ($720 billion) by 2030, making up a significant chunk of India's total lending space.

It represents nearly 55% of the total ₹10.8K lakh crore digital lending market opportunity in the country, with GenZ and millennials driving this charge.

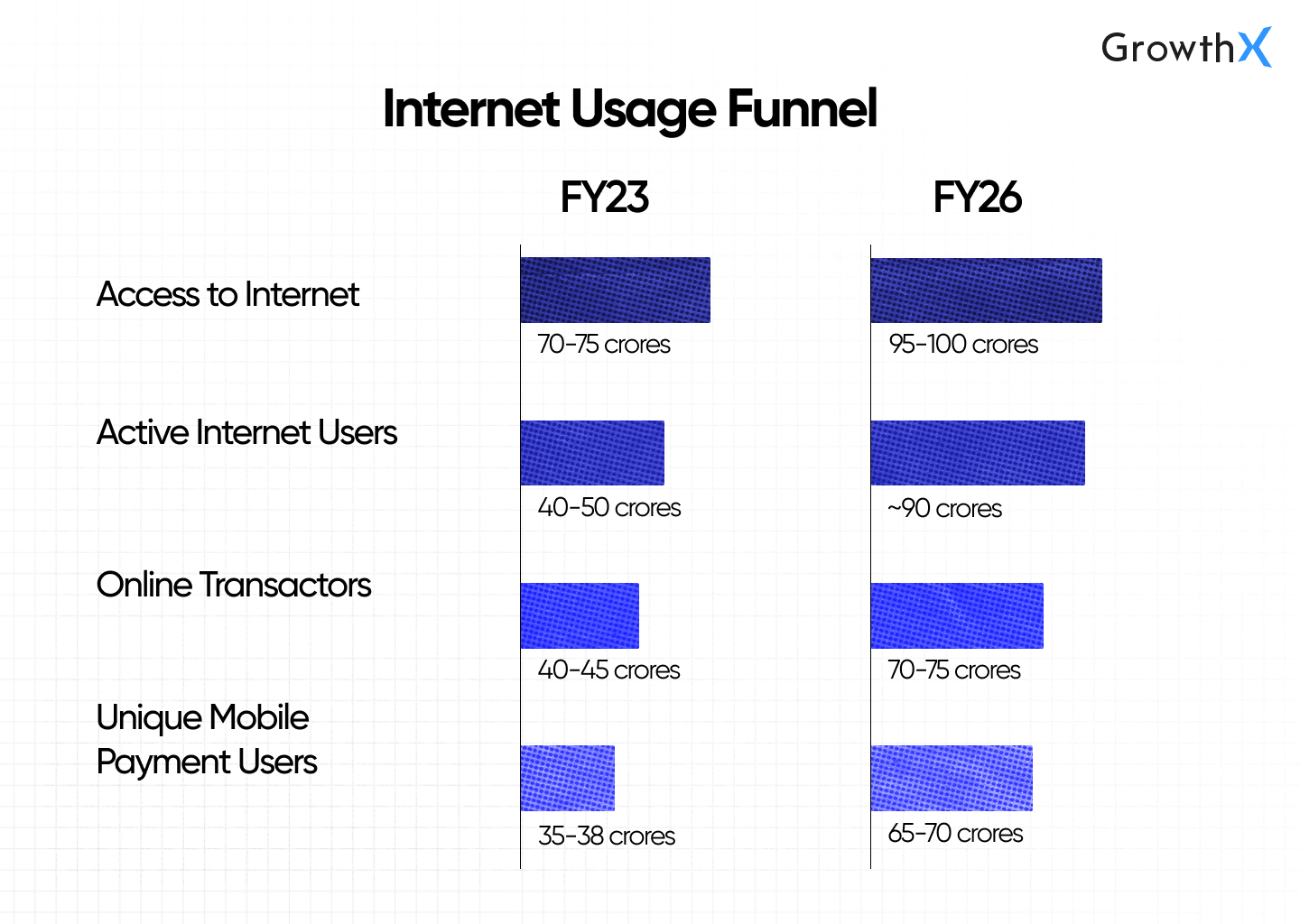

Digital Payments

Digital payments in India are skyrocketing, with transaction value jumping roughly 58% in a single year, going from ~₹7200 crore to ~₹11,400 crore 🤯

For FY23-24, digital payments for retail hit a whopping ₹299 lakh crores ($3.6 trillion)

UPI accounted for more than 75% of the total transaction volume of India’s retail digital payments in February 2023.

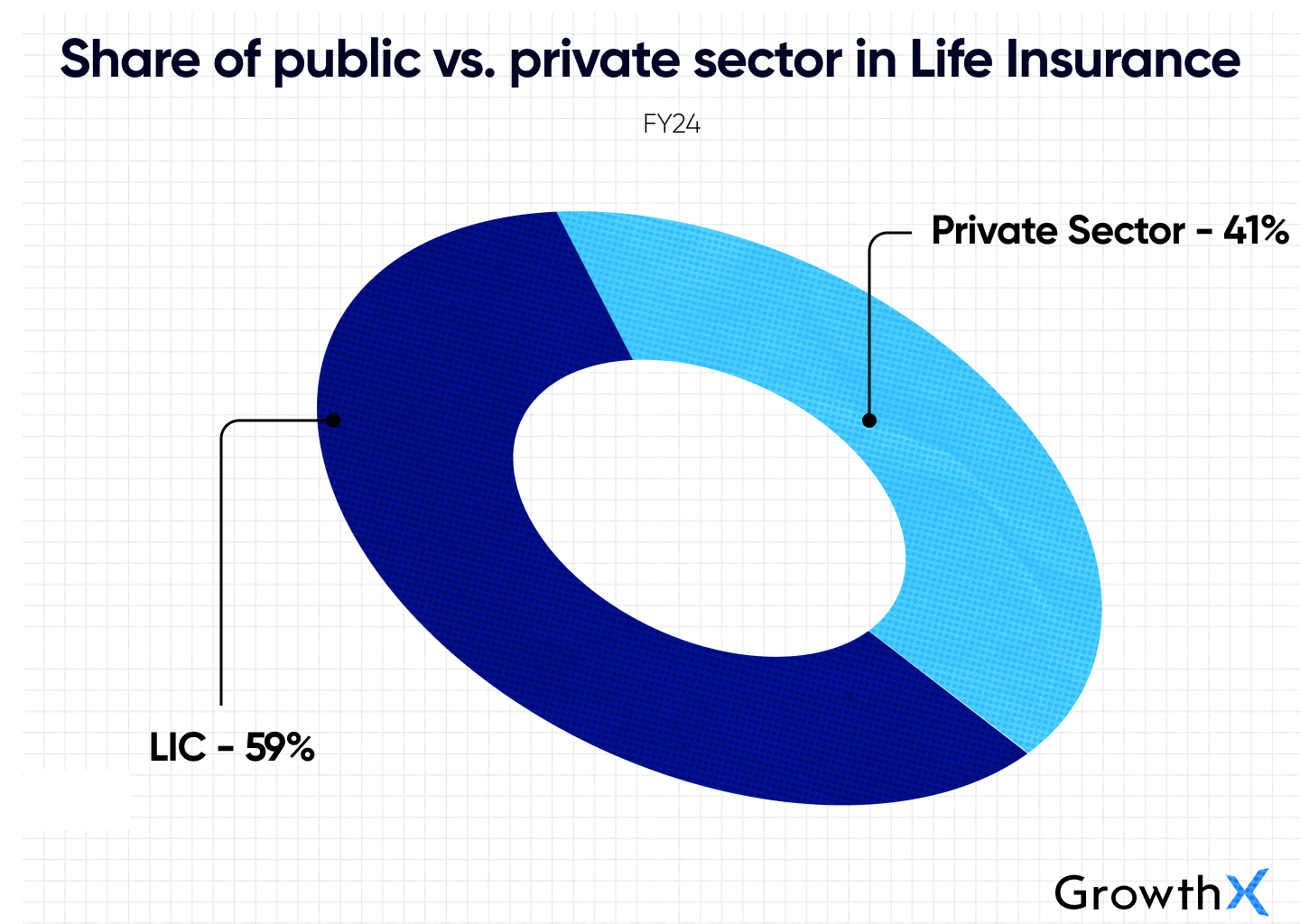

Insurance

India’s insurance industry is growing rapidly, thanks to rising incomes and greater awareness.

It's now the fifth-largest life insurance market among emerging economies, expanding at 32-34% annually.

While insurance penetration is at 4%, below the global average of 6.8% the sector is set to grow, with the insurance tech market expected to reach roughly $88 billion by 2028.

Market Trends

1. India's Fintech Boom 💥

India’s fintech market is exploding, surging past ₹66K crore ($80 billion) in 2023 and set to reach a staggering ₹83 lakh crore ($1 trillion) by 2030.

→ The country is a global hotspot, ranking fourth in fintech funding worldwide and second in the Asia-Pacific region.

→ The first quarter of 2024 alone saw fintech funding jump 59% from the previous quarter, highlighting the sector's strong momentum.

2. RBI’s New PA-CB Regulation ⚠️

The Reserve Bank of India’s PA-CB Regulation introduced in late 2023 is tightening the reins on fintech 🙃

Non-bank Payment Aggregators and Payment Gateways (PA-CB) now face direct RBI oversight, requiring a minimum net worth of ₹15 crore and a path to ₹25 crore within three years. This marks a significant shift in regulatory expectations, increasing the entry barriers for new players.

3. Digital Lending & BNPL Growth 📈

BNPL is becoming a go-to option for Gen Z and millennials, enabling them to make big-ticket purchases with ease.

Major e-marketplaces like Amazon are integrating these lending options directly at checkout, further boosting adoption. Interestingly, BNPL is also making inroads into the B2B space, offering businesses more flexible payment terms ⚡️

4. Peer to Peer and Peer to Merchant Transactions 🫂

In the first half of 2023, P2P transactions jumped 22% to roughly 23 billion, while their value surged 41% to approximately ₹64 lakh crore

Despite a slight decrease in the average ticket size for all UPI transactions, P2P transactions saw a 15% increase in ATS, indicating higher-value transactions among peers.

5. Rise of Co branded Credit Cards 💳

Co-branded credit cards are growing at a CAGR of 35-40% and could account for over 25% in terms of issuance by FY28!!

Crazy right?

Now if you want to dive deeper into this booming market, you can check out our GrowthX Insider video, where Vikash Singh, Director of Growth at Flipkart and an OIR at GrowthX, shares GTM strategies and key insights about the co-branded credit card industry👇🏻

Competitive Landscape 🥊

Last year, a few of our members from GX16 chose CRED as their capstone project, focusing on doubling its revenue from ₹1200 Cr to ₹2400 Cr and driving over 20% of users to adopt at least one monetisable feature.

You can also join the membership to solve growth challenges organically, connect with professionals in business, marketing, product, and more.

Scale your revenue and expand market share with our structured approach.

We’re an invite-only community of 3000+ members, who are product, marketing, and business leaders, and founders from top internet-first companies like Google, Canva, CRED, Stripe, Netflix, and more 💎

Now, let’s dive into the competitive landscape for CRED, leveraging the insights from our members' project!

Note - All insights are based on 2023 data and are subject to change.

CRED

CRED’s core value proposition is that is an exclusive credit card bill payment platform in India that offers rewards to its members when they pay their credit card bills promptly.

Keeping this in mind - despite it having a breadth of products – we selected Paytm, PhonePe, Cheq and traditional banking portals – that allow users to pay their credit card bills.

1. PayTM

- Core Value Proposition: One-stop solution for all your digital payment needs. With Paytm, you can make payments quickly and easily at millions of merchants across India.

- Positioning in the Market: Convenient and affordable, given its positioning it has a wide reach across India covering low-tier towns.

- Product Features

→ Core Feature: Payments through UPI, Digital Wallets

→ Sub Features/Products: Recharges and Bill Payments, Mutual Fund Investment, Equities Trading, Book Flights and Trains, Credit Cards, Buy Insurance, E-Commerce (Paytm Mall and ONDC), Savings Bank Account.

- Monthly Active Users: 89 million

- Advantage over CRED:

→ Larger user base.

→ Direct cashbacks in the wallet.

- Disadvantage over CRED:

→ Less loyal customer base.

→ Complicated UI/UX with numerous features on the first fold.

- Point of Differentiation:

→ CRED has a niche offering for responsible credit card management and rewards, while PayTM primarily focuses on digital payments and offers a wide range of services.

→ Has the top-tier users of India (by incomes brackets) which spend more on digital products and are easily monetisable

2. PhonePe

- Core Value Proposition: Comprehensive app for payments, gold purchases, investments, and more.

- Positioning in the Market: Positioning itself as a convenient and affordable way to make a variety of payments, money transfers etc.

- Product Features:

→ Core Feature: Payments through UPI

→ Sub Features/Products: Mobile Recharge and Bill Payments, Online Shopping, Buying Insurance, Investments (Mutual Funds), Loans, Online Ticket Booking, Bill Splitting, Savings and Rewards, Booking Trains and Flights.

- Monthly Active Users: 165 million

- Advantage over CRED:

→ Larger user base.

→ Direct cashback in the wallet.

- Disadvantage over CRED:

→ CRED has a more convenient UI and one-click payment. PhonePe is complicated with too many products and low discoverability.

→ Inferior design and experience

- Point of Differentiation:

→ Superior UI/UX in credit card management.

→ Better rewards system.

3. Cheq

- Core Value Proposition: Credit card bill repayment platform with credit score tracking and cashback rewards.

- Positioning in the Market: One-stop shop for credit-related services, including bill payments and credit score tracking.

- Product Features:

→ Core Feature: Paying credit card bills

→ Sub Features/Products: Credit Score Checking, Rewards Program (1% cashback through vouchers), Spend Analysis.

- Monthly Active Users: 7, 00,000

- Advantage over CRED:

→ Cashback can be redeemed for vouchers.

→ Allows combined payments for credit card bills in one transaction.

- Disadvantage over CRED:

→ Charges a flat Rs 100 processing fee for credit card repayments.

→ Limited offers compared to CRED.

- Point of Differentiation:

→ Superior UI/UX.

→ Better offers and no transaction fee for credit card payments

→ Several CRED users shifted to Cheq, but churned and came back after the rewards program went bad.

4. Traditional Banking Portals (HDFC, ICICI, Axis, SBI)

- Core Value Proposition: Manage all banking needs, including credit card bill payments.

- Positioning in the Market: Legacy method for managing credit card bills with evolving mobile apps.

- Product Features:

→ Core Feature: Comprehensive banking services

→ Sub Features/Products: Personal Loans, Utility or Rent Payments, Credit Card Bill Payments.

- Advantage over CRED:

→ Captive set of audience who still prefer to pay their CC bills via banking web/mobile app due to habit and trust built-in.

- Disadvantage over CRED:

→ Complicated UI/UX, often desktop-first.

→ No reminders

→ Doesn’t store card details for other bank cards, although you can still pay them

- Point of Differentiation:

→ Superior UI/UX.

→ Provides reminders and stores credit card details

→ Scans CC bill and highlights hidden/wrong charges

2. CRED Cash

Context 🧠

→ CRED Cash is a service that allows you to access quick, hassle-free credit directly from the CRED app, offering instant funds when you need them, without the usual paperwork or delays.

→ Given CRED Cash is the biggest source of revenue for CRED it is also important to study its competitive landscape

Competitor Analysis for CRED Cash 👇

(P.S: You can scroll these tables from right to left for more metrics)

ㅤ | Minimum loan amount | Maximum loan amount | Minimum Interest | Processing fee | Criteria | Documentation | Disbursal Time | Minimum Payment Tenure | Loan book size (In Cr) | Partial Payments (above existing EMI) |

CRED Cash | 5,000 | 5,00,000 | 12% | 1-4% | Minimum Score of 750 | No KYC | 30 minutes | 1 month | 10,000 | Not allowed |

Bajaj Finserv | 20,000 | 40,00,000 | 11% | 3.93% + a flexi fee of around 0.7% | Minimum score 685 | Everything (PAN, Aadhar, salary slip for last 3 months, bank statements, etc.) | 1-2 days | 1 month | 67,000+ | Allowed with charges of 4.72%.

If the loan is a “ Flexi term loan “or“ Flexi hybrid loan”, part pay is allowed |

HDFC Bank | 50,000 | 40,00,000 | 10.5% | 1.5% of the loan amount or 4500, whichever is higher | Minimum score of 700 | Everything (PAN, Aadhar, salary slip for last 3 months, bank statements, etc.) | 3-7 days | 1 year | 1,71,000+ | Allowed with charges of 2-4% (depending on tenure) of part payment amount |

Navi | 10,000 | 20,00,000 | 9.9% | 4-6% (min 1500 and max 7500) | Minimum score 650 | PAN and Aadhar | 20 minutes | 6 months | 7141 | Allowed with no extra charges |

Money View | 5,000 | 5,00,000 | 16% | 2-5% | Minimum score 600 | PAN, Aadhar, bank statements | 1-2 days | 3 months | 6400 | Allowed with charges of 4.72%. If the loan is a “ Flexi term loan “ or “ Flexi hybrid loan”, part pay is allowed |

3. Others

Here’s the Competitive Landscape of some other markets that CRED operates 👇

(Click on them for more insights!!)

CRED Mint 🔄

Context 🧠

→ CRED Mint is a feature that lets you earn high returns by lending your money to trustworthy borrowers within the CRED community, making your idle funds work smarter for you.

(P.S: You can scroll this table below from right to left for more metrics)

Competitor | Interest Rate Given | Minimum Investment Amount | Time to Invest | No. of Investors | Current AUM | Play Store Rating | Withdrawal Condition |

Cred Mint | 9% | 1,00,000 | 5 minutes | 61000 | 1000 Cr | 4.5 | Anytime, amount credited in T+1 |

LiquiLoans | Upto 10.5% | 10,000 | 1 hour | 13200 | 3700 Cr | 2.8 | Anytime, amount credited in T+3 |

LenDen Club | Upto 12% | 10,000 | 1 hour | 9100000 | 12000 Cr | 4.2 | Anytime, amount credited in T+1 |

LendBox | Upto 14% | 10,000 | 1 hour | 330000 | 1900 Cr | 3.2 | Anytime, amount credited in T+1 |

IndiaP2P | Upto 16% | 5000 | 1 hour | NA | NA | NA | 12 month lock-in, 2% premature withdrawal fees |

MobiKwik | Upto 12% | 1000 | 1 hour | 150000 | 2100 Cr | 4.3 | Anytime, amount credited in T+1 |

CRED Flash (BNPL) 🧾

Context 🧠

→ CRED Flash is a deferred payments facility acting as a personal loan offered by CRED in partnership with specific lenders.

1. CRED

- Core Value Proposition: Makes credit management easy and rewarding for creditworthy individuals with features like credit card bill payment, rewards, exclusive financial products, and community access.

- Monthly Active Users: 16 million

- Advantage Over Competitors: Specializes in credit card management, offers comprehensive rewards, and has exclusive partnerships.

- Disadvantage: Smaller user base compared to some competitors.

- Point of Differentiation: Focuses on responsible credit card usage and rewards users for timely payments.

2. PayTM Postpaid

- Core Value Proposition: One-stop digital payment solution with rewards and high security.

- Monthly Active Users: 89 million

- Advantage Over CRED: Larger user base, greater reach, and brand awareness.

- Disadvantage Over CRED: Less loyal customer base, less specialization in credit management.

- Point of Differentiation: Broad digital payment services vs. CRED’s specialized credit card management and rewards.

3. Slice

- Core Value Proposition: Virtual credit card and buy-now-pay-later service with rewards.

- Monthly Active Users: 5 million

- Advantage Over CRED: Offers a virtual credit card for online and offline purchases.

- Disadvantage Over CRED: Less comprehensive features and partnerships.

- Point of Differentiation: Focuses on young professionals with virtual credit card services, while CRED offers broader financial management.

4. Mobikwik Zip

- Core Value Proposition: Simple and rewarding digital payments with a wide merchant network.

- Monthly Active Users: 20 million

- Advantage Over CRED: Larger user and merchant base.

- Disadvantage Over CRED: More general-purpose platform, less specialized.

- Point of Differentiation: Primarily a digital wallet, whereas CRED focuses on enhancing the credit card experience.

5. Amazon Pay Later

- Core Value Proposition: Seamless payments integrated with Amazon and beyond.

- Monthly Active Users: 300 million+

- Advantage Over CRED: Huge user base and integration with Amazon’s e-commerce platform.

- Disadvantage Over CRED: Lacks exclusive brand partnerships available on CRED.

- Point of Differentiation: Strong integration with Amazon’s ecosystem vs. CRED’s focus on credit card management.

6. Zest Money

- Core Value Proposition: Buy-now-pay-later with flexible installment plans.

- Monthly Active Users: 10 million

- Advantage Over CRED: Allows splitting purchases into up to 12-month installments.

- Disadvantage Over CRED: Higher risk of bad debt due to less creditworthy users.

- Point of Differentiation: EMI solutions vs. CRED’s zero-interest EMI for one-month repayments.

7. Lazy Pay

- Core Value Proposition: Interest-free pay-later option.

- Monthly Active Users: 3 million

- Advantage Over CRED: Interest-free payments with no fees.

- Disadvantage Over CRED: Relies on late payment fines; less trust compared to CRED’s focus on maintaining user credit ratings.

- Point of Differentiation: Makes money from late payments vs. CRED’s transaction fees and trust-focused model.

CRED Escapes 🧳

Context 🧠

→ Cred Travel is a travel platform launched by CRED in March 2023.

→ It offers a curated selection of luxury and premium stays at over 300 hotels and resorts in over 50 domestic and international destinations.

1. CRED Travel

- Core Value Proposition: Curated luxury and premium stays with exclusive perks, benefits, and effortless travel planning.

- Average Package Price (Excluding Flight): ₹50,000

- Average Trip Length: 2-3 days

- Average Cost per Day: ₹20,000 - ₹30,000 per night

2. MakeMyTrip

- Core Value Proposition: One-stop travel shop with customization options, deals, and discounts.

- Average Package Price (Excluding Flight): ₹60,000

- Average Trip Length: 5-7 days

- Average Cost per Day: ₹5,000 - ₹15,000 per night

3. Yatra

- Core Value Proposition: Wide inventory, excellent customer support, and flexible stay options.

- Average Package Price (Excluding Flight): ₹60,000

- Average Trip Length: 5-7 days

- Average Cost per Day: ₹5,000 - ₹15,000 per night

4. Cleartrip

- Core Value Proposition: Simple booking process with express booking features and exclusive deals.

- Average Package Price (Excluding Flight): ₹60,000

- Average Trip Length: 5-7 days

- Average Cost per Day: ₹5,000 - ₹15,000 per night

4. Booking.com

- Core Value Proposition: Vast selection of accommodations, verified reviews, and flexible booking options.

- Average Package Price (Excluding Flight): ₹60,000

- Average Trip Length: 5-7 days

- Average Cost per Day: ₹5,000 - ₹15,000 per night

5. Airbnb

- Core Value Proposition: Unique stays with host interaction and local experiences.

- Average Package Price (Excluding Flight): ₹20,000

- Average Trip Length: 2-3 days

- Average Cost per Day: ₹3,000 - ₹10,000 per night

CRED Garage 🚘

Context 🧠

→ CRED’s monetisation for CRED Garage is by selling motor vehicle insurances to its users for who renewals are due.

→ CRED earns a commission fee of 25-28% on the policy amount. IRADAI has an upper limit of 20% on the commission the broker (in this case CRED) can avail from the insurance provider. 5-8% is the marketing commission charged by CRED.

CRED only earns commission if it switches the user from the current insurer to a new insurer

ㅤ | Ease of Renewal process | Post sale assistance | Pros | Cons |

CRED | No | Instant | Extra credit card benefits + amazing UI/UX | Processing fees and allowing only 1 rental payment per month |

Acko | No | Instant | Platform associated with house rental and purchases - hence rental payment feels natural | Processing fees & all cards not accepted |

PolicyBazaar | No | Instant | Instant and habit already formed | Not possible to pay through credit card, hence opportunity cost of reward points |

Insurancedekho | Yes | 1-2 days | Processing Fee is low | Cumbersome process to sign up and the payment processing time is too high |

ICICI | No | Instant | Allows payments for shop owners, and allows more than 1 rental payment per month | Processing Fees, all cards not accepted |

Market Share

How does CRED make money? 💰

CRED offers a myriad of services and it’s easy to get confused as to which ones make money for CRED.

To understand them better let’s categorise them into two areas

1. Finance Sub-Products

Sub Products | Core Value Prop | Pros and Cons | Competitors | Does it earn money for CRED? |

CRED Pay | Scan and Pay via UPI

Quick and safe

Pay-and-checkout option for e-commerce | Pros: Pre saved cards, faster checkout, higher cashbacks, superior user interface

Cons: For UPI, not a familiar UI while paying to local and street vendors | PayU, CCAvenue, Google Pay, PhonePe, Paytm | Yes (the payment gateway) ✅

CRED earns revenue in this category through a payment aggregation fee |

CRED Cash | Personal loan up to 5 lakhs with instant and paperless disbursement | Quick disbursement, No documents, Zero foreclosure charges | All banks and NBFCs

Paytm, CASHe, MoneyTap, Navi | Yes ✅

CRED charges a 1-2% fee on loans facilitated and distributed by CRED Cash. |

CRED Mint | Investment in P2P loans given to credit worthy CRED users. Users get up to 9% per annum on their investments

Partnered with Liquiloans to power this | Positive: Only lends to CRED users, more trust

Negative: Lower IRR than competition | LenDen Club, 12% Club, Liquiloans, Mobikwik, Faircent, IndiaP2P | Yes ✅ |

CRED Flash | BNPL product –

Allows the user to pay back within 30 days at zero interest. Option available to users with high credit rating only | One step checkout on commerce stores

Can manage payments on one app along with credit cards

| Lazypay, Simpl, Zest Money, Bajaj Finance, PostPe | Yes ✅

|

Bill payments –CRED Rent, educational fees, other bill payments | Pay Home or Office Rent, Deposit, Maintenance, Pre paid recharge, Postpaid bills, DTH, Broadband, Landline bills, Gas, Water, Electricity, School fees, University fees etc. | Fast, Smooth

Negative: 1%-1.5% extra charge and no points for credit cards on rent payments | Netbanking, UPI apps. | Yes ✅

Convenience Fee |

2. Lifestyle Sub-Products

Sub Products | Core Value Prop | Positives & Negatives | Competitors | Does it earn money for CRED? |

CRED Store | A curated e-commerce store to purchase homegrown D2C brands at a discount by using the accumulated CRED coins | Positive: Discovery-led, fresh new brands, great deals

Negative: Brands are small, keep changing, a power user cannot repeat previous orders, for some products pricing on Amazon is low | Amazon, Flipkart, Instagram | Yes ✅

Service fees from merchants, payment aggregation fee, advertisement Fee |

CRED Escapes | Curated travel experiences with exclusive discounts in luxurious locations – both international and domestic. Users can use CRED coins for discounted prices | Positive: Carefully selected packages at good rates

Negative: Low flexibility, Expensive locations, Good deals available only during shoulder season | MMT Black, Luxury Escapes, Booking.com | Yes ✅

Earns a commission from travel partners |

Gamified Rewards and Brand Vouchers | Exciting rewards and vouchers of brands where users can avail discounts or free products by playing games on CRED | Positive: Addictive games (Especially slot machines)

Negative: Vouchers are usually from brands irrelevant to the user, no reminders on expiry | CashKaro, Dealshare, Groupon | Yes ✅ |

Cred Garage | It offers a one-stop solution for car services like repairs, insurance, and documentation, ensuring high transparency, quality, and convenience. | Positive: Extra credit card benefits + amazing UI/UX

Negative: Processing fees and allowing only 1 rental payment per month | Acko, Policybazaar, Insurancedekho, ICICI | Yes ✅

Insurance Commission |

The depth you see here is just a feeler of the depth we teach at GrowthX 💫

GrowthX is an invite-only club of over 3000 members who are product, marketing, and business leaders, and founders from top internet-first companies like Google, Canva, CRED, Stripe, Netflix, and more 💎

We teach our members how to scale revenues via frameworks that can be applied starting next Monday morning. The GrowthX Membership is built on 3 core pillars:

1. Learning experience: Where you learn the science of revenue-led growth with frameworks actionable the next Monday morning.

2. Curated community: Where you access a safe space for you to soundboard anything that is stressing you at work.

3. Career outcomes: Over 35% of members are founders & are able to hire growth teams to scale revenue for their companies while operators are able to get into breakout leadership roles.

Explore GrowthX Membership 🏆

Cost Levers 💸

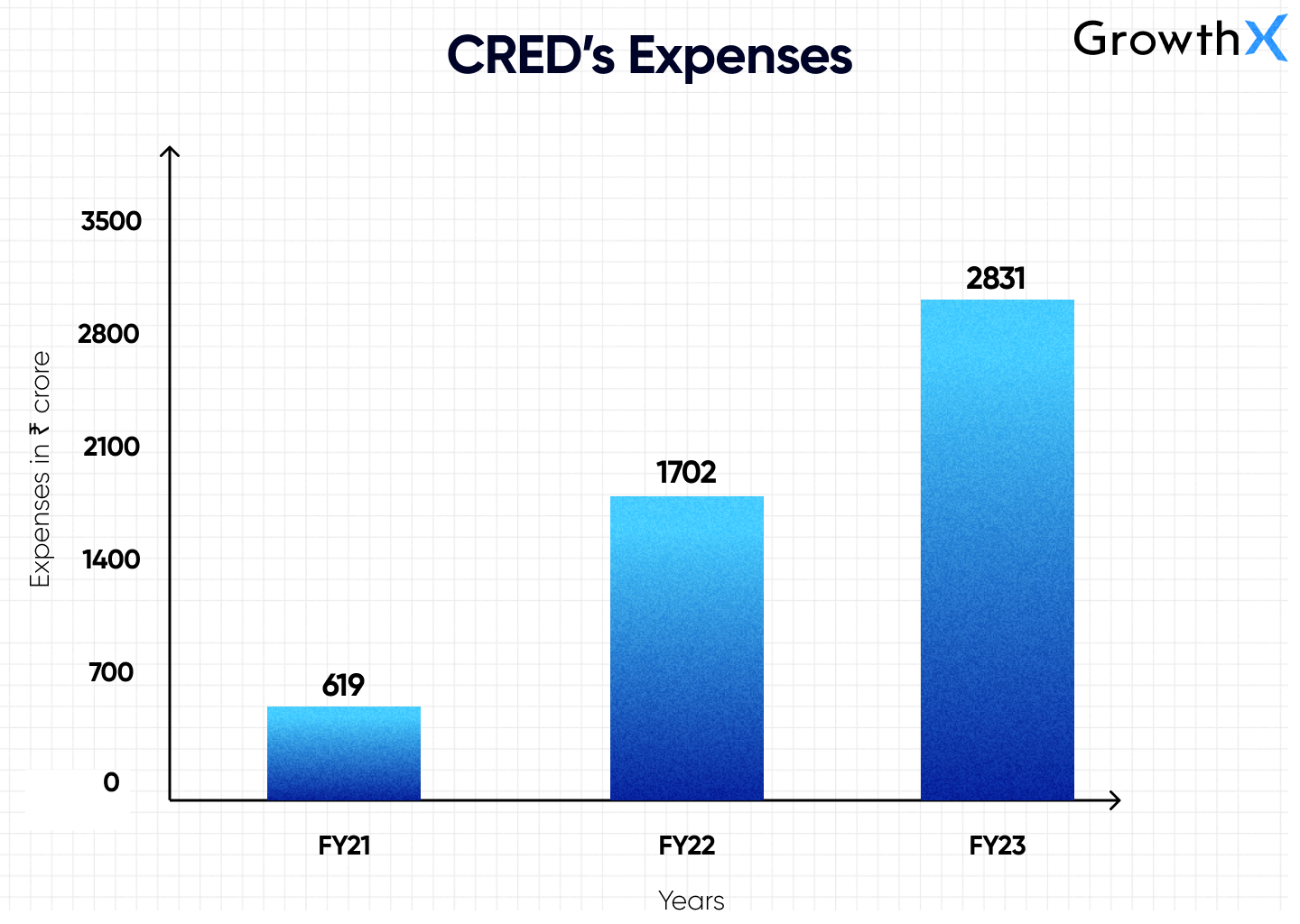

1. Customer Acquisition (CAC): Marketing, promotions, and referral programs to attract and retain high-value users.

CRED spent a whopping ₹713 crores on marketing in 2023 alone! 🤯

If you've seen the ad with Rahul Dravid being Indiranagar ka Gunda, you know they've got game with their Influencer Marketing campaigns.

Similar to CRED, if you're aiming to leverage "influence" as a powerful driver of customer acquisition and revenue for your organisation, we’ve got something special for you. 💫

FREE Influence Selection Foundations by GrowthX 🚀

This guide is your playbook for picking the right influencers and strategically aligning your product with channels that maximize ROI.

Ready to elevate your brand’s influence and drive results?

2. Employee Benefits: Significant costs tied to salaries, benefits, and incentives to retain talent.

3. Technology & Development: Continuous investment in app development, backend infrastructure, and security systems to maintain a smooth user experience

4. Compliance & Regulation: Expenses for meeting legal and regulatory requirements, particularly in data privacy and financial services.

5. Credit Risk Management: Managing lending risks, including defaults and fraud.

6. Operational Expenses: General overheads such as office space, utilities, and customer support operations.

7. Rewards & Cashback Programs: Funding for loyalty rewards and incentives, which are central to CRED's user engagement strategy.

Market Opportunity

1. Wealth Management for Affluent Users

With the booming growth in India’s high-net-worth segment and the rising trend of investors seeking tech-driven, personalised financial advice, CRED can leverage its acquisition of Kuvera to offer premium, tailored investment solutions.

This would position CRED as a key player in India’s wealth tech space, directly competing with traditional financial advisors.

2. Exclusive Health & Wellness Partnerships

Health and wellness are increasingly important to high-net-worth individuals.

CRED can tap into this by forming strategic partnerships with premium fitness and wellness brands, offering exclusive access to high-end services, retreats, and products.

This move would not only enhance the lifestyle appeal of the CRED platform but also deepen user engagement through unique, value-added experiences.

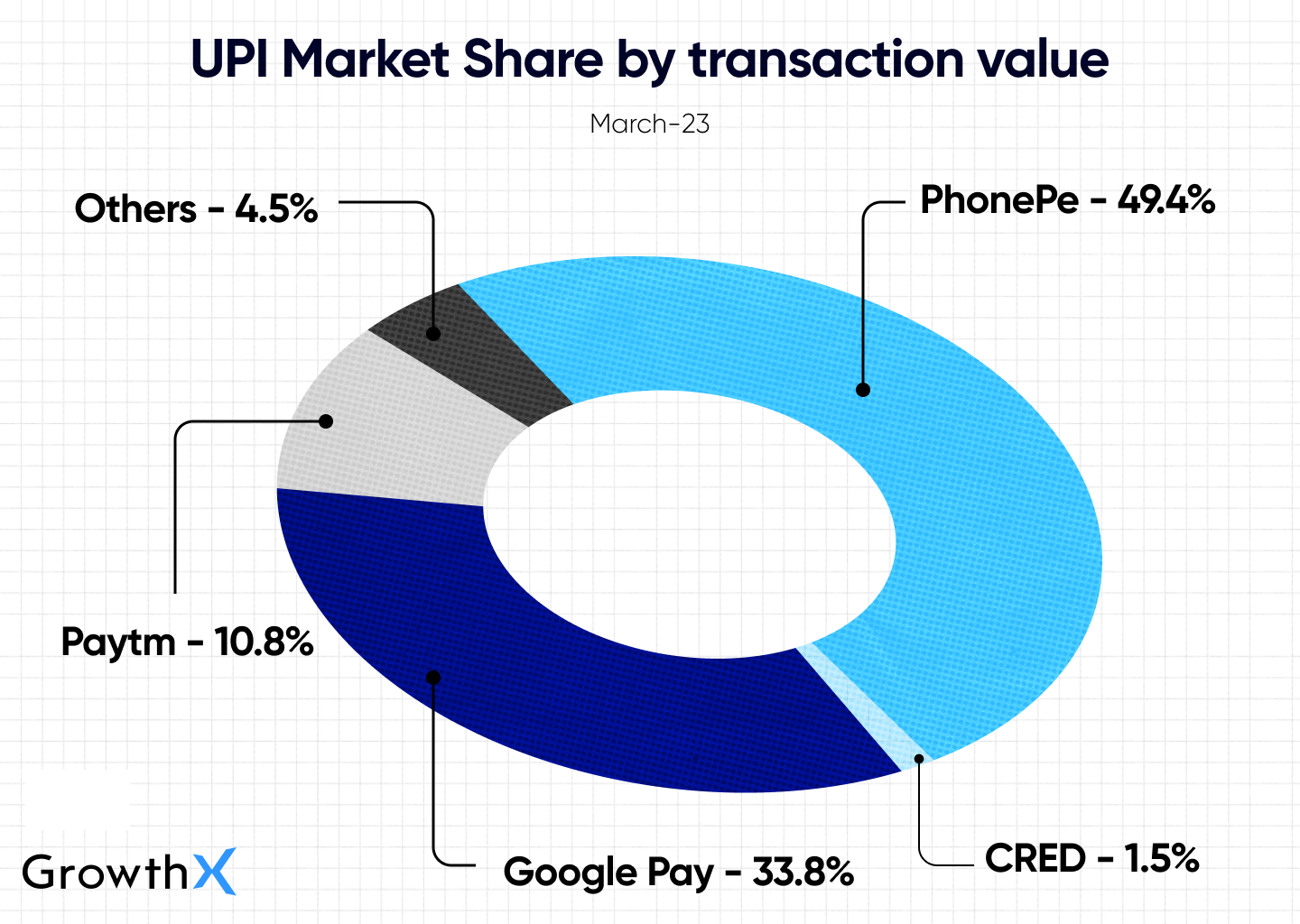

3. Expanding into UPI with a Competitive Edge

With Google Pay and PhonePe controlling around 85% of the UPI market, CRED has a prime opportunity to disrupt the space.

Despite the National Payments Corporation of India (NPCI) considering revisiting its 30% market share cap by the end of 2024, CRED can still capitalise on this potential shift.

By integrating more deeply into the UPI ecosystem and offering innovative, user-centric features, CRED has the chance to carve out a significant portion of this market, leveraging its strong user base to boost transaction volume and drive substantial growth.

Challenges

1. Regulatory Challenges

The RBI’s latest guidelines are stirring things up for apps like CRED, PhonePe, and Paytm.

Starting July 1, credit card payments through third-party apps must go through the Bharat Bill Payment System (BBPS).

If your bank hasn’t linked up with BBPS yet, these apps won’t work for your bill payments. Big names like HDFC and ICICI are affected, meaning users will need to switch to bank apps or even go old-school with branch payments.

For fintech players like CRED, this is a tough hit, forcing them to rethink their strategies.

2. Expanding Beyond Top-Tier Customers

CRED is shifting its focus from its usual high-credit-score users to target a broader audience, including those new to credit. This move, while necessary for growth, brings significant challenges.

The top 30 million credit-savvy users in India are limited in number and not as eager for credit, making it tough for CRED to scale with them alone.

To tap into the larger, untapped market of new-to-credit users, CRED plans to use Prefr, a platform acquired through CreditVidya, and Newtap Technologies, its in-house lending arm.

However, this expansion into a new customer base with less predictable credit behaviour introduces higher risks associated with potential defaults, which could impact the platform's reputation and financial stability.

3. CRED’s Premium-to-Mass Market Pivot

CRED Store, once known for its high-end exclusivity, is moving into mass-market territory. While it could boost sales, there’s a risk—diluting its premium brand.

Brands that once flaunted their CRED presence might rethink their partnership as the store shifts focus.

By the way, we have much more value in store for you 💫

FREE in-depth play books on some of the core problems you might be struggling with at work.

These are not hacks but deep-actionable frameworks built by the Learning & Experience team at GrowthX.

You can access foundations on 👇

5. SEO

6. Monetisation