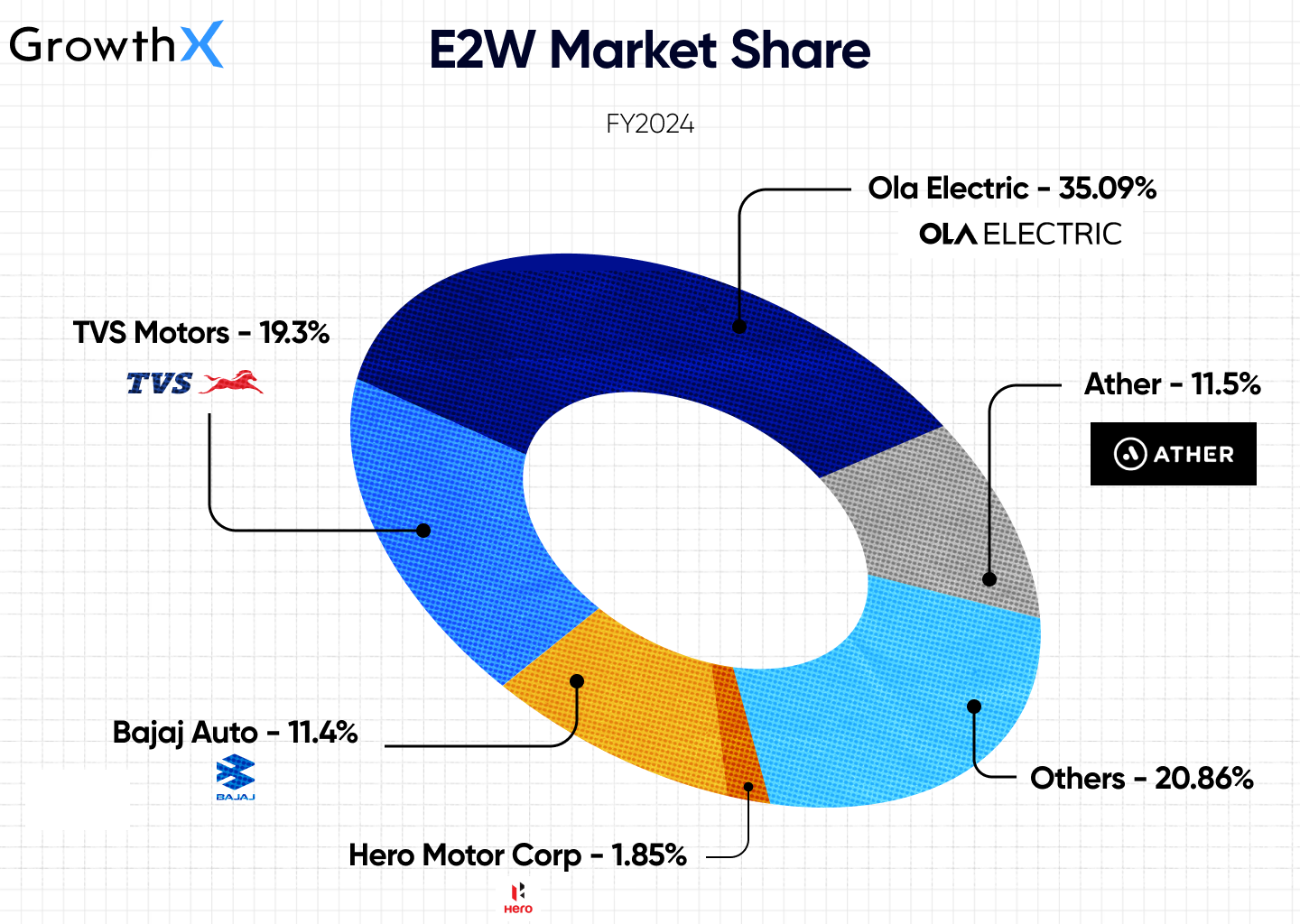

Ather Energy's business model revolutionises India’s electric vehicle landscape, starting with the launch of the Ather S340 in 2016. Founded by IIT Madras graduates, their focus on smart technology and strategic partnerships, including a ₹205 crore investment from Hero MotoCorp, led to the Ather 450’s success. By 2024, Ather boasts an 11.5% market share and over ₹1,700 crore in revenue.

The story of Ather Energy began in 2013 when two IIT Madras students, Tarun Mehta and Swapnil Jain, set out to revolutionize electric vehicles (EVs) in India.

Initially exploring energy solutions like battery swapping, they soon realised the core problem was poorly designed electric vehicles.

This led them to a bold decision: rather than just making batteries, they would create India's first smart electric scooter 💫

Inspired by Tesla, they aimed to build a scooter better than petrol vehicles, both in performance and design.

So in 2016, Ather introduced the S340, a breakthrough with a touchscreen dashboard and connected features at a technology conference Surge in Bengaluru, which was the first step towards transforming India's E2W market into a smart and sustainable mobility ecosystem 🌏

But building an EV from scratch in India was no small feat. They faced significant challenges, especially when it came to sourcing quality parts from local vendors who weren't equipped to meet Ather’s high standards - causing delays in production.

But the turning point came when Hero MotoCorp invested ₹205 crores, providing the capital and industry connections required to scale.

So in 2018, Ather launched the Ather 450, India's fastest electric scooter at the time 🤯

By 2021, thanks to cost-cutting measures and strategic partnerships with industry giants like Hero, Ather was finally able to achieve positive gross margins.

Ather wasn’t content with just being another scooter company—they wanted to change the game entirely. They introduced industry-first features like the Ather Grid, a fast-charging network, and their proprietary AtherStack software, offering over-the-air updates, ride statistics, and cloud integration.

In 2024, they launched the 'Rizta' series, targeting the family scooter market with features like 56L of storage space and an industry-first traction control system.

🚀

Fast forward to 2024, Ather Energy has firmly established itself as a leader in India’s electric two-wheeler (E2W) market with

11.5% market share

Annual revenue of over ₹1,700 crore.

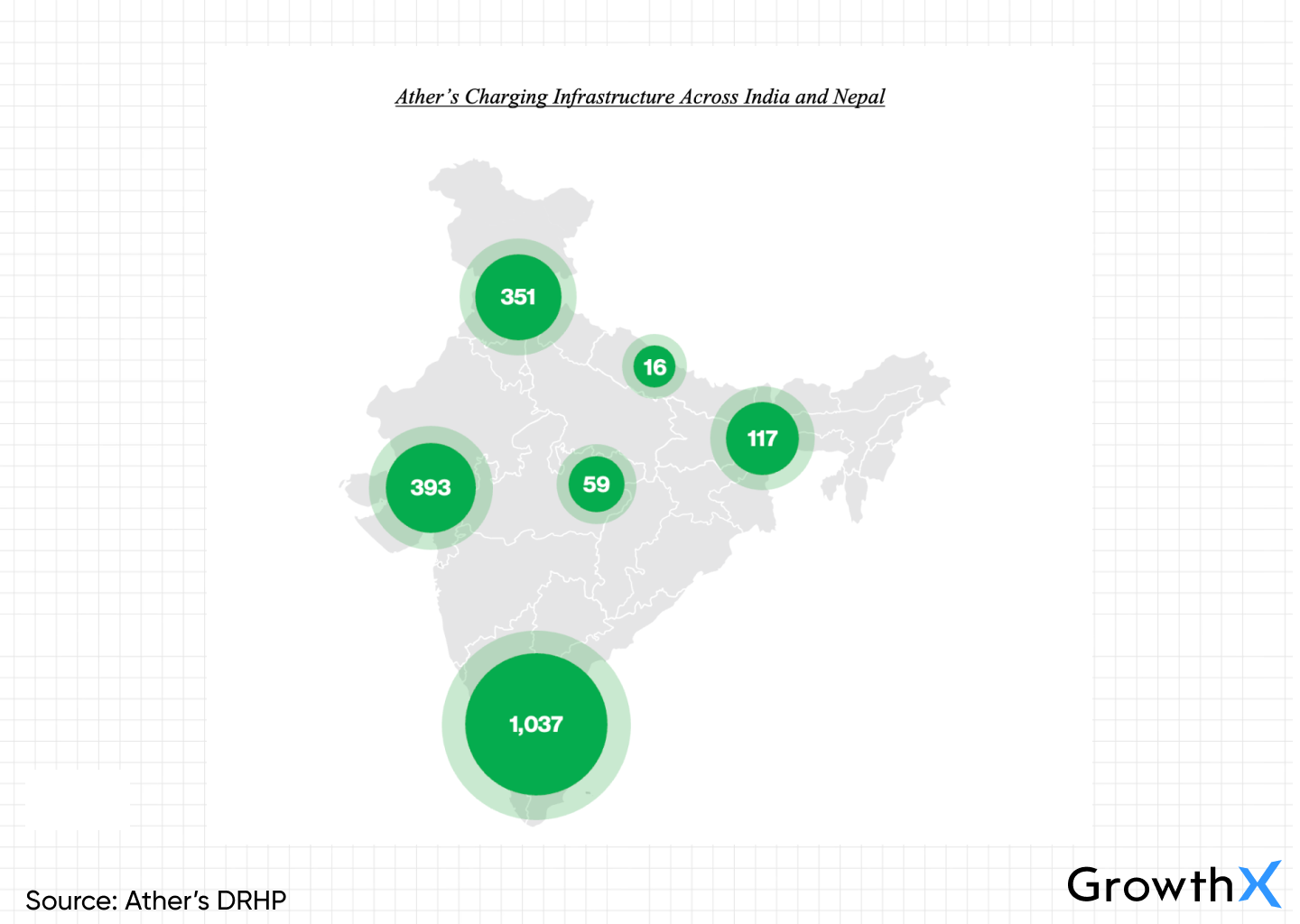

With over 2,500 chargers across 230 cities and

With a dealer network spanning 208 Experience Centers in 154 cities (plus expansion into Nepal)

Ather’s MOAT (Competitive Advantage)

1. First Mover Advantage 🏁

Ather didn’t have the luxury of relying on an existing brand or network like TVS, Bajaj, or Ola.

Instead, they built everything from scratch, setting a new benchmark for electric two-wheelers (E2W).

They were the first to bring cutting-edge tech into scooters and by that we mean

→ The first touchscreen dashboard

→ The first scooter with Android

→ The first scooter with Google Maps navigation through WhatsApp and yes, they added a 4G SIM card, paying for the data themselves!

And the list doesn’t end here.

Back in 2018, Ather launched the Ather 450, an electric scooter with a top speed of 80 km/h, matching ICE scooters—an industry first.

They kept pushing the boundaries with more innovations like fast charging, cloud integration, and even OTA software updates—something no one else in India’s E2W market had.

Because they were the first to deliver premium, high-quality electric scooters, they captured the attention (and wallets) of early adopters. This has solidified their reputation for premium quality, even as more players enter the market.

💡

By the way, the depth you see here is just a feeler of the depth we teach at GrowthX 💫

GrowthX is an invite-only club of over 3000 members who are product, marketing, and business leaders, and founders from top internet-first companies like Google, Canva, CRED, Stripe, Netflix, and more 💎

We teach our members how to scale revenues via frameworks that can be applied starting next Monday morning. The GrowthX Membership is built on 3 core pillars:

1. Learning experience: Where you learn the science of revenue-led growth with frameworks actionable the next Monday morning.

2. Curated community: Where you access a safe space for you to soundboard anything that is stressing you at work.

3. Career outcomes: Over 35% of members are founders & are able to hire growth teams to scale revenue for their companies while operators are able to get into breakout leadership roles.

Explore GrowthX Membership 🏆

2. Largest Charging Network 🔌

One of the biggest challenges for EV owners is charging anxiety.

Apparently 51% of EV owners in India considered switching back to petrol or diesel vehicles because of charging concerns, high maintenance costs, and low resale values.

Ather addressed this head-on by creating Ather Grid, India's largest E2W fast-charging network.

🔋

By June 2024, India's overall charger-to-EV ratio stood at 1:252, way below the ideal 1:10 needed for smooth operations.

However, Ather’s wide network of 2500+ chargers in 230+ cities helps ease this concern, giving their customers confidence in the ability to charge on the go.

By establishing their own fast-charging network early, Ather has removed one of the largest barriers to EV adoption.

They even partnered with places like petrol pumps, cafes, and restaurants to expand access, and with Google Maps, users can now find Ather Grid chargers directly.

This massive infrastructure footprint gives Ather a significant competitive edge over newer entrants.

What makes it even better?

Ather has open-sourced their charging standard (LECCS), which has now become a national standard. That means their fast chargers are compatible with other EVs too. In short, they’ve made EV charging easier for everyone—setting themselves apart from the competition.

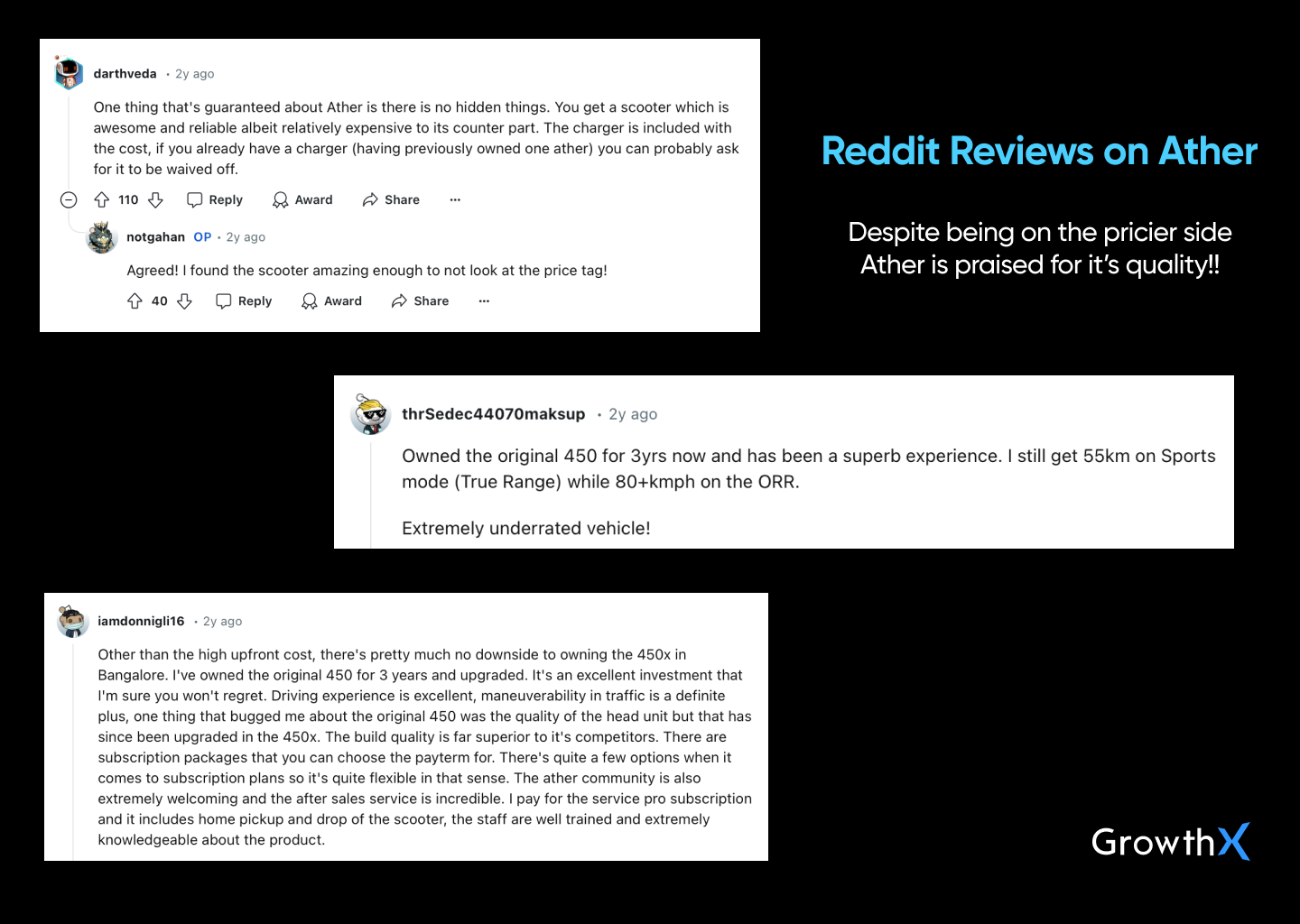

3. Word of Mouth 🗣️

Even without flashy marketing campaigns, Ather has earned a strong reputation purely by delivering top-notch quality.

When they started, early adopters wanted premium scooters, and Ather was the brand that delivered. Despite their higher price point, their scooters were the go-to choice, especially when competitors like Ola were in the news for quality issues like battery fires.

Their customers became brand ambassadors, spreading the word about Ather’s reliability and performance.

And while bigger players like TVS, Bajaj, and Ola may have more visibility, Ather’s focus on building a loyal customer base through quality has paid off 👏🏼

Market Overview

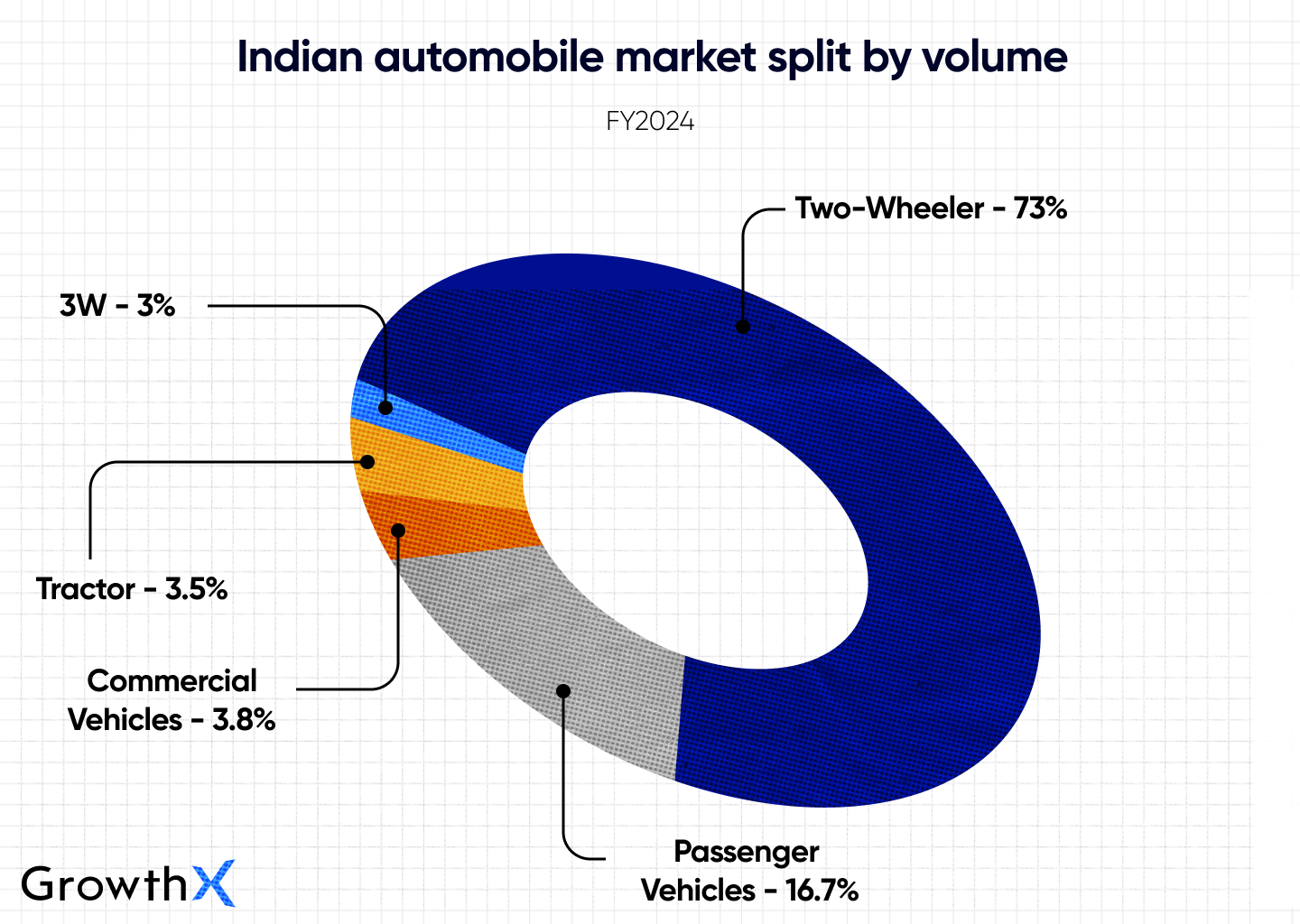

The Indian two-wheeler (2W) market dominates the country’s automotive sector, accounting for over 70% of all registered vehicles.

This strong existing infrastructure and consumer familiarity with two-wheelers make them an ideal starting point for electrification.

🏍️

The segment sold 8.4 lakh electric two-wheelers (E2Ws) in CY23, marking a 33% year-on-year (YoY) growth, even after a 25% subsidy cut in June.

E2Ws have gained significant traction, with every 2nd EV sold in India being a two-wheeler!!

As India is the second-largest two-wheeler market globally, this segment is witnessing a rapid shift towards electric mobility.

Scooters 🛵

Scooters, particularly in the 90cc-125cc range, have witnessed growing demand due to their convenience and suitability for both men and women in urban environments.

The segment’s market share grew from 31.7% in FY19 to 34.2% in FY24, with a notable shift towards higher cc models. Convenience scooters, primarily in the 110cc and 125cc categories, dominate the market.

Scooters lead the electric two-wheeler market, especially in the premium segment where 75% of sales are electric.

Motorcycles 🏍️

Although motorcycles remain the dominant two-wheeler type in India, their share of the market has slightly decreased in favour of scooters.

There has been a notable shift towards higher-capacity motorcycles, with the 125cc segment growing by 11% CAGR from FY19 to FY24.

So what is causing this growth? 🤔

2W Penetration - 2W penetration increased from 106 per 1,000 people in FY19 to 116-118 in FY24.

🌟

The segment's popularity spans across various economic classes:

👉🏻 63% of middle-class households own two-wheelers.

👉🏻 Even among affluent households, 75% own a two-wheeler.

Replacement Demand: Despite rising interest in cars, the affordability gap and stagnant income growth in certain segments mean many two-wheeler owners continue to upgrade within this category, especially toward higher-capacity models (≥125cc).

Urbanisation: As cities expand, demand for personal mobility rises. 2W, especially scooters, are preferred due to their convenience in congested urban environments and growing usage in delivery services.

Government Policies: Strong incentives, like FAME I & II, GST reductions, and state subsidies, have accelerated the shift to electric two-wheelers. The E2W market saw a 101% CAGR from FY19 to FY24.

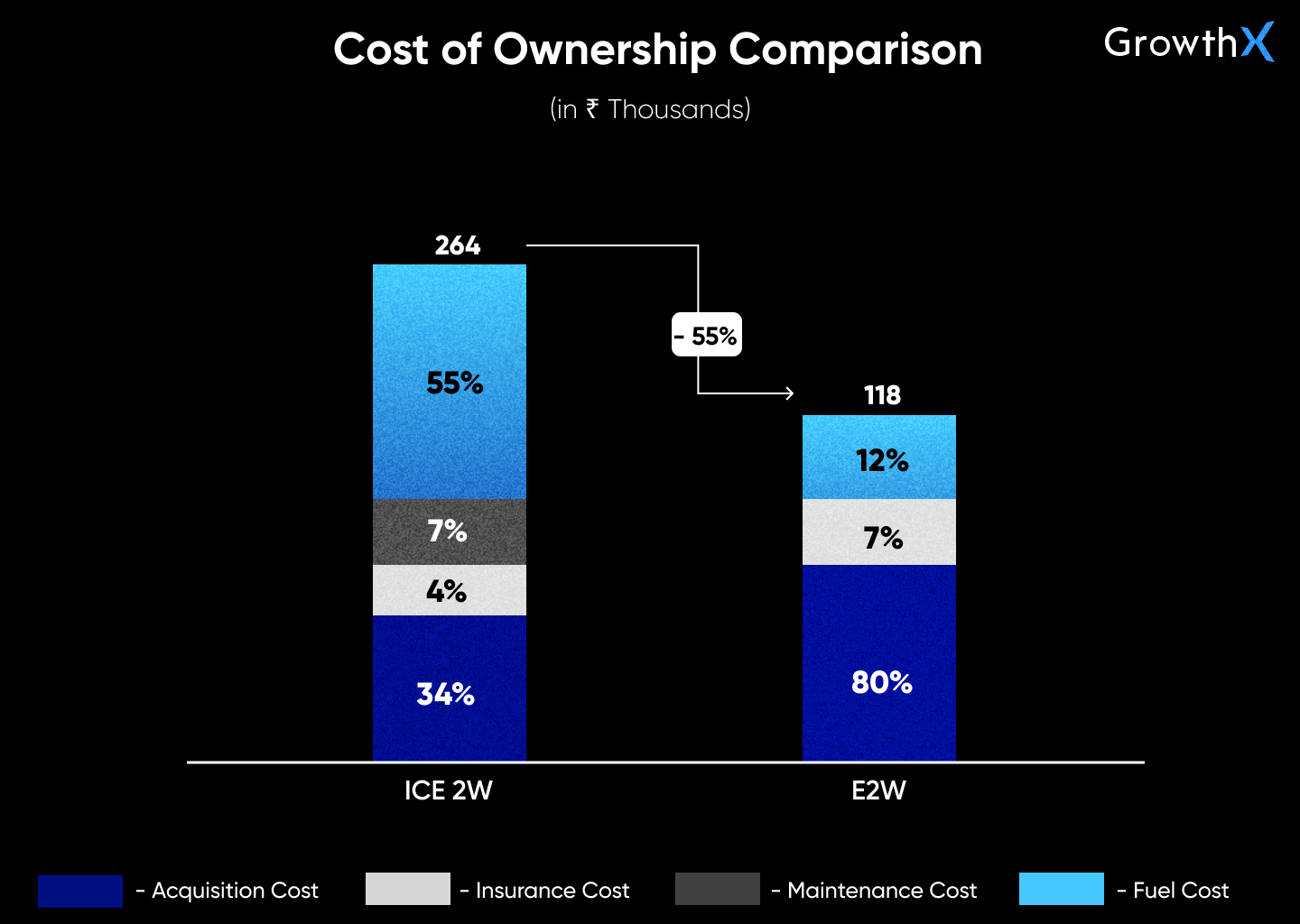

Fuel Prices & TCO: Rising fuel costs have heightened the appeal of E2Ws due to their lower total cost of ownership (TCO). For example, electric two-wheelers in India are about 45% cheaper to own over their lifespan compared to their gasoline-powered counterparts. This trend is more pronounced in urban areas with higher pollution and congestion.

The increasing participation of women in the Indian workforce has provided a significant boost to scooter sales. Scooters are popular among working women due to their ease of use, lighter weight, and greater maneuverability. As female workforce participation grows, it is expected to contribute further to the growth of the two-wheeler industry, particularly in the scooter segment.

2. Premiumisation Trend in Two-Wheelers

A shift towards premium motorcycles and scooters is evident, with customers upgrading to vehicles with higher engine capacities and better features.

📌

From 2019 to 2024

→ the share of motorcycles with engines ≥125cc rose from 38% to 52%

→ while similar growth was seen in scooters, where vehicles ≥125cc grew from 20% to 47%.

Younger consumers, higher disposable incomes, and improved financing have driven this premiumisation trend, which mirrors similar trends in other industries, such as consumer electronics and passenger vehicles.

3. Changing Dealership Landscape in the Two-Wheeler Market

The rise of E2Ws has introduced a new dealership model in the two-wheeler industry: the company-owned-company-operated (COCO) model.

In this model, OEMs manage their own outlets, controlling inventory, sales, and after-sales services. This contrasts with the traditional dealer-owned-dealer-operated (DODO) model, where independent dealers handle these aspects.

As the market for E2Ws grows, the COCO model is expected to expand, offering OEMs more control and direct customer engagement.

4. Rising Investments and Export Potential

👩🏻💻

India’s large and young workforce, along with government support for manufacturing, is drawing more investments into the automotive sector. In fact, private capital expenditure in the automotive industry grew by 4-5% in FY 2023.

India is also ramping up its vehicle exports. In FY 2023, about 18% of the vehicles produced in India were exported, and this number is likely to grow as the country strengthens its position as a global manufacturing hub.

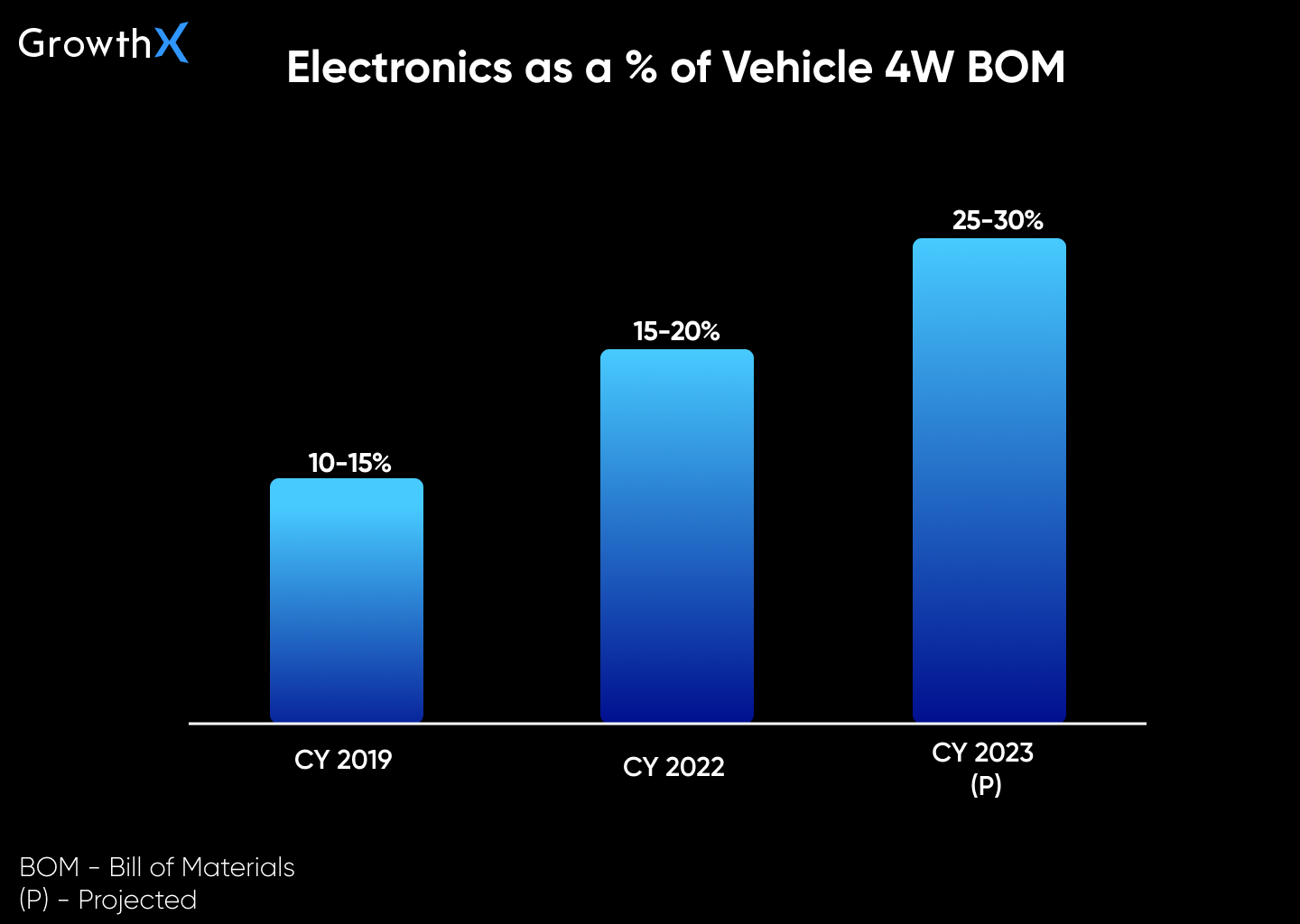

5. Vehicles Becoming 'Computers on Wheels'

As drivers demand more safety, comfort, and performance, vehicles are becoming increasingly reliant on electronics and software.

Safety features are now standard, and the cost of electronics in vehicles is expected to make up 25-30% of a car's cost by 2030, reflecting the shift towards more advanced, electrified vehicles.

Competitive Landscape

1. Ola Electric Mobility Limited

Founded: 2017

Models: Ola S1 Pro (Gen 1), Ola S1 Pro (Gen 2), Ola S1, Ola S1 Air, Ola S1 X+

Revenue: ₹5,009 crore (FY24)

Revenue Mix: Dominated by vehicle sales (91.89%), with a small portion from non-vehicle sales (8.11%).

Key Points:

→ Leading E2W Market Share -Grew by 115% YoY, recording its highest monthly volume of 53,000 units in March 2024.

→ Extensive network with 870 experience centers and 431 service centers across India.

→ Introduced Ola Care and Care+ programs for free home servicing, theft assistance, and towing services.

→ Battery Warranty: 8-year/80,000 km, plus access to 248 hyper chargers and 764 standard chargers for fast charging (50 km in 15 minutes).

2. TVS Motor Company

Founded: 1962

E2W Models: iQube ST, iQube, iQube S, TVS X

Revenue: ₹3,91,447 million

Revenue Mix: Primarily from vehicle sales (75.35%), with a notable contribution from non-vehicle segments (24.65%).

Key Points:

→ Fourth-largest Two-wheeler manufacturer in the world

→ Partnered with 24M Technologies to build a factory in India, targeting the energy storage and electric mobility markets.

→ 2nd largest E2W player by volume in FY24, with sales growing 120% to reach 183,205 units.

→ Extensive distribution network with 700+ dealers across 400+ cities.

→ Partnered with Tata Power and Jio BP for charging infrastructure, supporting 2,000+ public chargers.

→ Launched SmartXonnect, a suite of connected features, and offers roadside assistance for 1 year.

💡

By the way, the depth you see here is just a feeler of the depth we teach at GrowthX 💫

GrowthX is an invite-only club of over 3000 members who are product, marketing, and business leaders, and founders from top internet-first companies like Google, Canva, CRED, Stripe, Netflix, and more 💎

We teach our members how to scale revenues via frameworks that can be applied starting next Monday morning. The GrowthX Membership is built on 3 core pillars:

1. Learning experience: Where you learn the science of revenue-led growth with frameworks actionable the next Monday morning.

2. Curated community: Where you access a safe space for you to soundboard anything that is stressing you at work.

3. Career outcomes: Over 35% of members are founders & are able to hire growth teams to scale revenue for their companies while operators are able to get into breakout leadership roles.

Explore GrowthX Membership 🏆

→ Established Chetak Technology Limited (CTL) in 2021, a 100% subsidiary of Bajaj Auto, to focus on electric two-wheelers.

→ Sales Growth: From 3,000 units in March 2023 to 16,000 units in March 2024, with total sales crossing 1 lakh units in FY24 (4x growth YoY).

→ Expanded distribution to 204 dealers in 160 cities.

→ Value-added features include navigation, reverse mode, and TecPac with a 3-year/50,000 km warranty.

→ Focus on expanding charging infrastructure with onboard and offboard charging options.

4. Hero MotoCorp

Founded: 1984

Models: V1 Plus, V1 Pro

Revenue: ₹3,77,886 million

Revenue Mix: Primarily vehicle sales driven (84.83%), with some revenue from non-vehicle sales (15.17%).

Key Points:

→ Plans to expand its EV offerings by launching three new electric scooters in 2024 targeting various market segments.

→ Currently holds a smaller share of the market but is focusing on long-term growth and international expansion, especially in Latin America.

→ Expanded its sales channel to over 100 cities and 150 dealers by leveraging Hero dealer network

🤝🏻

Hero MotoCorp owns 40.89% of Ather Energy on a fully diluted basis.

5. Eicher Motors

Founded: 1948

Revenue: ₹1,65,358 million

Revenue Mix: Primarily vehicle sales driven (75.70%), with some revenue from non-vehicle sales (24.30%).

Key points:

Royal Enfield, India’s leading motorcycle manufacturer in the middleweight segment, is going towards the electric vehicle (EV) strategy.

With 25-30% of Royal Enfield’s Rs 1,000 crore capital allocation for FY24 going towards electric vehicles

Royal Enfield revealed its first EV, Electric Himalayan, at the 2023 EICMA Motor Show.

The launch is planned for India in 2025, aiming to capture market share in the premium electric bike segment.

Market share

Revenue Model

Ather Energy generated a total revenue of ₹1,753.8 crore (₹17,538 million) in FY24. Let’s break down their revenue streams into simple categories

1. Electric Scooter Sales (E2Ws)

This is the primary source of Ather Energy’s revenue, accounting for a significant portion of the company’s income.

Ather’s electric two-wheelers (E2Ws), like the Ather 450X, are the backbone of their business. In FY24, sales of these finished goods contributed to 90% of the revenue.

Model

Sales Volume (2024)

Revenue Contribution as a % of revenue from operations

Revenue (₹ crore)

Ather 450X

39,067

34%

590.5

Ather 450X (3.7 kWh)

35,999

31%

535.5

Ather 450S

22,712

16%

277.7

Ather 450X (2.9 kWh)

11,249

9%

157.8

Ather 450 Apex

550

1%

9.1

2. Vehicle Accessories and Stock-in-Trade

In addition to selling electric scooters, Ather also generates revenue from EV-related accessories, spare parts, and merchandise.

This includes items like helmets, chargers, and other add-ons.

Until April 2023, portable chargers were also sold as stock-in-trade. After this date, they began selling chargers bundled with their E2Ws. This contributed to 3% of revenue from operations

3. Services

Ather Energy provides several services related to its scooters, most notably through its Pro Pack, which includes Atherstack features, three years of access to Ather Connect, and an extended battery warranty.

Continued subscriptions to Ather Connect and other after-sales services also contribute to their revenue. This chunk makes up 7% of revenue from operations.

4. Other Operating Revenue

Ather derives other minor sources of income, primarily through the sale of scrap materials. Although small, this contributes to the company’s overall operating revenue — with a percentage contribution of 0.2%

Cost Levers

1. Cost of Materials Consumed

This is Ather’s largest expense, covering raw materials and components used to manufacture their electric two-wheelers (E2Ws).

While some components like the chassis, battery management system (BMS), and motor controller are outsourced, Ather controls the design process.

😳

For FY24, the cost of materials represented 90% of their revenue from operations.

2. Purchase of Stock-in-Trade

Ather outsources the production of various accessories, spare parts, and merchandise (like TPMS sensors and chargers) from vendors.

The purchase of these stock-in-trade items accounted for 2% of their revenue from operations.

3. R&D Expenditure

Ather continues to invest heavily in research and development (R&D) to improve the design, technology, and user experience of their scooters and related infrastructure.

R&D costs cover both manpower (employees like engineers, designers, etc.) and non-manpower expenses (such as prototyping, testing, and software licenses).

R&D expenses as a percentage of total income amounted to 13% of total income

4. Employee Benefits

Employee benefits, including salaries, share-based payments, provident fund contributions, and other welfare expenses, are a major cost for Ather.

With over 1,400 on-roll employees and nearly 1,000 off-roll employees, this is a critical part of their expense structure.

5. Finance Costs

Ather incurs finance costs related to interest on borrowings and lease liabilities. These expenses arise from the company’s growth strategy and investments in infrastructure.

6. Other Expenses

Ather’s other expenses include marketing and promotional costs, brand-building activities, and various operational costs.

In FY24, they invested ₹907 million in marketing campaigns, focusing on initiatives like community outreach, test drives, and influencer marketing to enhance brand visibility.

💡

By the way, the depth you see here is just a feeler of the depth we teach at GrowthX 💫

GrowthX is an invite-only club of over 3000 members who are product, marketing, and business leaders, and founders from top internet-first companies like Google, Canva, CRED, Stripe, Netflix, and more 💎

We teach our members how to scale revenues via frameworks that can be applied starting next Monday morning. The GrowthX Membership is built on 3 core pillars:

1. Learning experience: Where you learn the science of revenue-led growth with frameworks actionable the next Monday morning.

2. Curated community: Where you access a safe space for you to soundboard anything that is stressing you at work.

3. Career outcomes: Over 35% of members are founders & are able to hire growth teams to scale revenue for their companies while operators are able to get into breakout leadership roles.

Explore GrowthX Membership 🏆

Market Opportunity

1. Expansion into Motorcycles & E3W 🚗

A. Motorcycles

Electric motorcycles in India have rapidly evolved, with startups pushing boundaries to create sleek, futuristic, and highly functional bikes.

Ather can tap into the same segment especially with range anxiety now being a thing of the past, with many models offering over 300 km on a single charge and acceleration from 0 to 40 or 60 km/h in just 3 seconds, making them ideal for everyday commuting.

B. E3W

The E3W segment in India represents an incredible growth opportunity.

🇮🇳

India has now become the largest market for electric three-wheelers, surpassing China with sales exceeding 5,80,000 units in 2023.

Globally, India's influence is evident, as one in every five three-wheelers sold worldwide in 2023 was electric, and nearly 60% of these were sold in India.

This growth is fueled by the thriving logistics and e-commerce sectors, which have accelerated the demand for electric cargo vehicles. Due to their rapid adoption Ather can tap into this market and get ahead of their competitors.

2. Export Potential & Premiumisation 📈

India’s influence in the global 2W market is not limited to domestic sales.

The country exported 3.5 million 2Ws in Fiscal Year 2024, representing 15-20% of its overall 2W sales, primarily to Africa, Asia, and North America.

As India is one of the largest 2W producers worldwide, Ather has a unique opportunity to leverage its manufacturing scale and export capabilities, and turn itself into a key player in the global E2W market.

🫶🏻

The rising middle class in India, which is expected to grow from 432 million to 715 million by Fiscal Year 2031, is driving a trend toward premiumisation in the 2W segment.

Since Ather positions itself as a major player catering premium E2W this provides them with ample market opportunity.

3. Government Support & Technological Advancements 📄

The Indian government has played a pivotal role in promoting EV adoption through initiatives like the National Electric Mobility Mission Plan (NEMMP) 2020 and the FAME scheme.

These policies, along with production-linked incentive (PLI) schemes and state-level subsidies, are making EVs more affordable and accessible, further accelerating their adoption.

With the cost gap between E2Ws and ICE 2Ws projected to reduce to about 7% by Fiscal Year 2031, the attractiveness of E2Ws is only set to increase.

Challenges

1. Marketing & Brand Awareness 📢

According to Ather's co-founder, Tarun Mehta, one of the biggest challenges the company faced was the lack of brand awareness.

With many consumers mistaking it for a foreign brand rather than a homegrown Indian company.

Despite increasing marketing spend in FY24, Ather has struggled in the highly competitive electric two-wheeler (E2W) market, where it lagged behind rivals.

🫣

For instance, Ather sold just about 3,000 scooters in FY20, while Ola Electric garnered 8,80,000 bookings in the first 12 hours of its launch!!

Even combining sales from FY19 to FY22, Ather's total fell short of Ola's pre-booking numbers.

Ather's early market entry was overshadowed by Ola's aggressive marketing and the established distribution networks of players like TVS and Bajaj, making it difficult for Ather to gain visibility and traction.

2. FAME Subsidy Reduction 🏷️

The reduction in the FAME-II subsidy for E2W in June 2023 posed a significant challenge for Ather.

⬇️

The government reduced the incentive per kWh and lowered the cap on subsidies from 40% to 15% of the vehicle's ex-factory price.

As a result, Ather's sales took a hit, especially in the three months ending June 30, 2024, compared to the same period the previous year.

If subsidies continue to decline, EVs could become less attractive to India's price-sensitive consumers, hurting Ather’s sales, especially as it competes against well-established internal combustion engine (ICE) vehicle manufacturers.

3. Premium Pricing Strategy 💰

Ather's decision to focus on the premium market has been both a strength and a challenge.

They have built top-quality scooters that customers love, but this premium positioning limited their appeal to a broader market.

In the early days, only early adopters were interested in electric scooters and were willing to pay a premium price. However, as the market matured, more consumers started looking for affordable options.

While Ather's commitment to quality earned them a loyal customer base, it also restricted their ability to capture the mass market, particularly as other brands like Ola Electric began to offer more competitively priced alternatives.

4. Capacity Utilisation 🏭

In Fiscal Year 2024, Ather's Hosur Factory operated at a capacity utilisation rate of just 29% across both their electric two-wheeler (E2W) assembly and battery pack manufacturing lines 🫤

The factory's total installed capacity was 4,20,000 units for E2W assembly and 3,79,800 for battery pack manufacturing per annum. They plan to expand battery pack manufacturing to 531,120 units per year are underway, but the low utilisation rate raises concerns.

If Ather is unable to boost demand and fully utilise this increased capacity, it risks missing out on the economies of scale that would help lower costs and improve margins.

Additionally, if Ather completes Phase 1 of Factory 3.0 and still fails to meet expected demand, it could face even greater inefficiencies, which would negatively impact their financial outlook.

📌

By the way, we have much more value in store for you 💫

FREE in-depth play books on some of the core problems you might be struggling with at work.

These are not hacks but deep-actionable frameworks built by the Learning & Experience team at GrowthX.