Table of Contents

- How was Netflix founded? 🎬

- Journey 🇮🇳

- Netflix’s MOAT

- 1. Content Differentiation

- 2. Affordability and Mobile-First Strategy

- 3. Brand Awareness and Cultural Penetration

- Market Overview

- State of Streaming 👩🏻💻

- Shrinking Subscriptions 🎟️

- But how are we watching? 📱

- The Rise of Regional Content 🌐

- Future Outlook for OTT Revenue 💰

- Competitive Landscape

- Market Share

- How does Netflix make money?

- Cost Levers

- Market Opportunity

- Challenges

Do not index

CTA Headline

CTA Description

CTA Button Link

How was Netflix founded? 🎬

It all started back in 1997. At the time, if you wanted to watch a movie, you’d head over to your local video rental store, and rent a VHS tape (A VHS is like a big, clunky black cassette tape for watching movies. Think of it as the 90s version of a DVD.) But this system had its flaws, like those annoying late fees you had to pay if you didn’t return the tape on time.

Reed Hastings, one of Netflix’s founders, felt this pain firsthand. He was charged a $40 late fee for a VHS rental of Apollo 13.

He was so frustrated with this, it made him think "What if there were no late fees?"

That simple idea lead to the birth of Netflix.

Along with his friend Marc Randolph, Hastings decided to start a movie rental service that wouldn’t charge people late fees. Instead of VHS tapes, which were too bulky and expensive to ship, they chose DVDs—a smaller, cheaper format, perfect for mail delivery. This innovation made Netflix possible as a mail-order DVD rental service, letting people rent movies from home.

In 1998, Netflix launched as a subscription-based service. Customers paid a flat monthly fee to rent DVDs, keep them as long as they wanted, and return them when ready for more. No late fees, just one monthly charge—a game-changer.

But Netflix wasn’t an instant success. Competing with Blockbuster, the rental giant, was tough. At one point, they tried selling Netflix to Blockbuster for $50 million, but that plan didn’t fall through.

By the 2000s, Netflix introduced something that would define its future: a movie recommendation system called Cinematch. This helped users discover films tailored to their tastes, making it easier to find what to watch next.

If you are interested in uncovering the business models of other internet-first companies, you can check out MakeMyTrip Business Model & other blogs here.

Journey 🇮🇳

By 2016, Netflix had evolved into a global streaming giant, reaching over 60 countries, with India next on its list.

On January 6, 2016, it launched in India, bringing its huge library for the Indian audience. However, Netflix faced a lot of hurdles: high pricing compared to local competitors like Hotstar, and a market used to cash payments.

However partnering with Paytm helped ease payment issues, and Netflix adapted by adding more Indian content.

Currently, Netflix:

- Has 10-12 million Indian subscribers

- Made ₹2,214 crore in revenue in 2023 (a 24% increase)

- Has a library of over 6,000 Indian and international titles.

- Is available in 35+ languages

Netflix’s MOAT

1. Content Differentiation

Netflix has made its mark by doing one thing really well: delivering content that’s both local and global.

Think of it like this: one moment you’re watching a gore-y crime series from India, next thing you know you’re switching to a quirky Spanish thriller. It’s all there, in one place.

They’ve mastered the art of turning local hits into global sensations. Remember Sacred Games? Netflix didn’t just serve it up to India—they took it worldwide. And with subtitles in over 35 languages, you could be watching a Turkish drama today and a French comedy tomorrow.

This strategy has helped Netflix increase its viewership by 30% in India over the last year.

2. Affordability and Mobile-First Strategy

India has a total of 918.19 Million internet subscribers in 2023, which accounts for ~50% of the Indian population and Netflix wanted to capitalise on that.

Here’s where the ₹149 mobile-only plan comes in. With 75% of OTT viewers using smartphones to watch, this plan was a game-changer. Netflix was suddenly way more accessible.

What’s the result?

Netflix saw a 30% increase in customer engagement and a 24% growth in revenue. It’s kind of like offering gourmet meals at street-food prices. Everyone's lining up for a taste, even in smaller towns.

Netflix became the "sachet-sized" premium content for India.

3. Brand Awareness and Cultural Penetration

In India, Netflix is synonymous with premium entertainment.

They were early to the game here, jumping in back in 2016 when the OTT space was still growing, and that early start has paid off.

It’s reached a point where “Netflix and chill” became a part of the culture. Even if they charge a bit more than some competitors, people stick around because it feels aspirational—like wearing your favourite brand.

Plus, with Netflix steadily increasing its licensed content by 6% this year, subscribers have more shows and movies to enjoy.

Bottom line here is that Netflix is the cool kid in the OTT world, and even though others are trying to catch up, Netflix has managed to keep its loyal fanbase by staying a step ahead with top-notch, irresistible content.

By the way, the depth you see here is just a feeler of the depth we teach at GrowthX 💫

GrowthX is an invite-only club of over 3000 members who are product, marketing, and business leaders, and founders from top internet-first companies like Google, Canva, CRED, Stripe, Netflix, and more 💎

We teach our members how to scale revenues via frameworks that can be applied starting next Monday morning. The GrowthX Membership is built on 3 core pillars:

1. Learning experience: Where you learn the science of revenue-led growth with frameworks actionable the next Monday morning.

2. Curated community: Where you access a safe space for you to soundboard anything that is stressing you at work.

3. Career outcomes: Over 35% of members are founders & are able to hire growth teams to scale revenue for their companies while operators are able to get into breakout leadership roles.

Explore GrowthX Membership 🏆

Market Overview

State of Streaming 👩🏻💻

Let’s talk Netflix and the streaming scene in India.

Right now, there are about 547.3 million people who could be watching online videos in India. But here’s the kicker: only 99.6 million of them are actually paying for subscriptions.

While the audience universe grew by 13.8% compared to 2023, this increase was entirely driven by the AVoD (advertising video-on-demand) segment, which grew by 21%, while the SVoD (subscription video-on-demand) segment saw a 2% decline.

Shrinking Subscriptions 🎟️

India still has 99.6 million active paid subscriptions, nearly identical to last year.

Even more telling, the average number of platforms subscribed to per paying user dropped from 2.8 to 2.5 in 2024.

This suggests a growing reluctance to pay for multiple streaming services as users consolidate their viewing habits.

But how are we watching? 📱

When it comes to devices, smartphones dominate the Indian OTT scene.

A whopping 97% of the audience uses their smartphones to watch online video content, and 81% rely solely on their phones for streaming.

However, connected TV is also gaining ground, with 69.7 million users consuming content via smart TVs, highlighting a shift in viewing preferences for larger screens.

The Rise of Regional Content 🌐

OTT platforms in India are increasingly catering to regional audiences.

By 2024, the share of regional language content is expected to double from 27% in 2020 to 54%, driven by more vernacular programming and films.

In 2021 alone, nearly half of OTT originals and 69% of films released were in languages other than Hindi. This trend reflects a broader shift towards localised content as platforms compete to capture the diverse Indian audience.

Future Outlook for OTT Revenue 💰

In terms of revenue, India’s OTT video market is projected to reach $4.06 billion in 2024, with an annual growth rate of 7.43% through 2029, potentially reaching $5.81 billion by that year.

Although SVoD is currently the largest revenue segment, contributing $2.02 billion in 2024, growth is slowing compared to AVoD. Meanwhile, global comparisons place the United States far ahead, with projected revenue of $132.9 billion in 2024.

By 2029, the OTT video market in India is expected to have 634.3 million users, with penetration rising to 42.2%. The average revenue per user (ARPU) is set to hit $8.26 in 2024.

Competitive Landscape

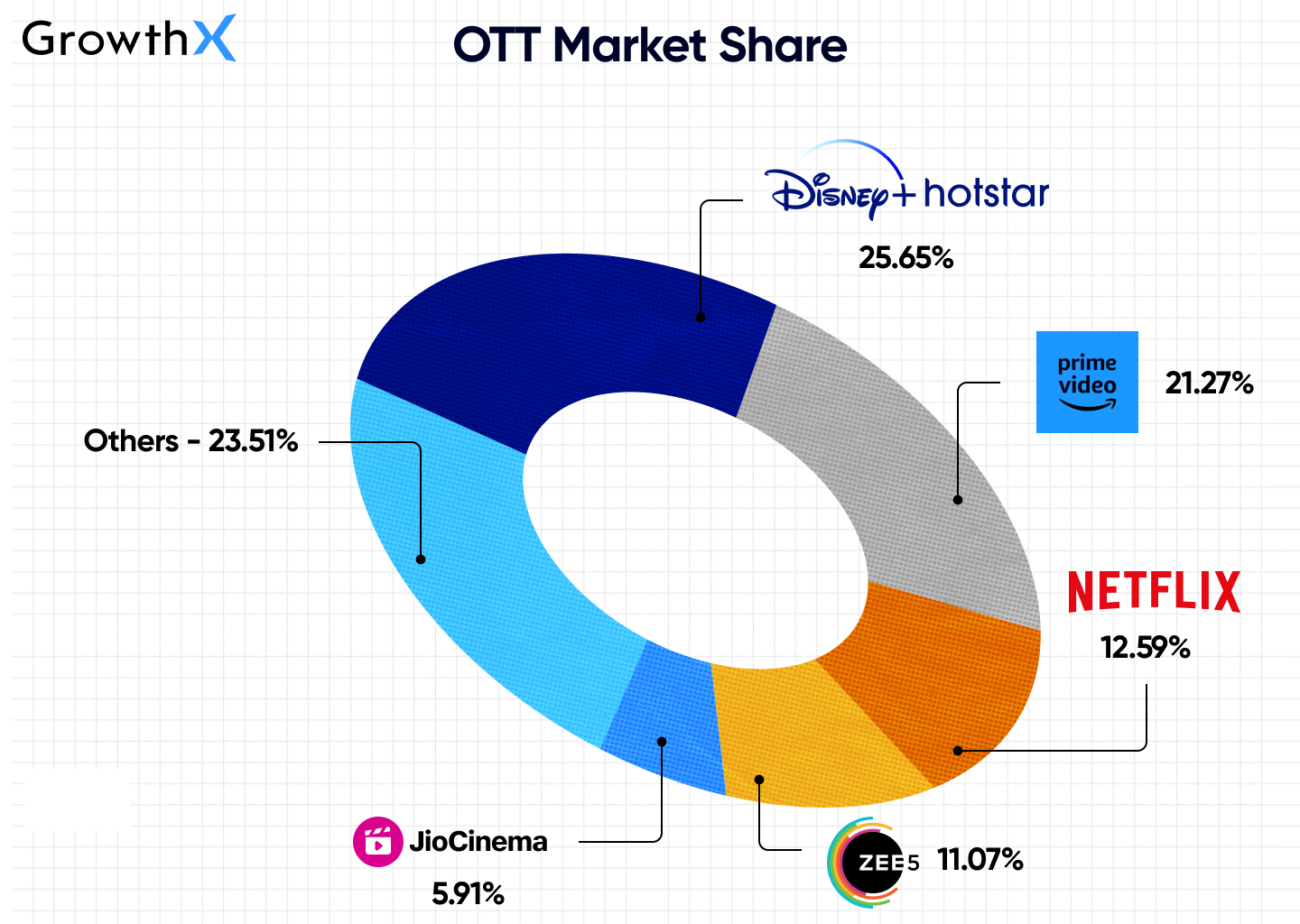

1. Disney+ Hotstar

Disney+ Hotstar, initially launched as Hotstar in 2015 by Star India, became a key player due to its combination of local content and live sports, especially cricket.

After Disney's acquisition of 21st Century Fox in 2019, Hotstar was rebranded as Disney+ Hotstar in 2020, merging global Disney content with its extensive Indian offerings.

- Gained traction through IPL and live sports; post-Disney acquisition integrated with Disney+ library (Marvel, Pixar, Star Wars)

- In 2024, Disney Star merged with Viacom18 (owned by Jio Platforms), bringing Disney+ Hotstar under the JioCinema ecosystem for expanded reach

- Subscriber base: 38.3 million

- Languages: Content available in 18 languages.

- Offers 1,00,000 hours of content

- Reach: 80% Reach in 1M+ towns & 50% reach contributed by the top 8 metros

- Pricing: ₹299 to ₹1499 with monthly, quarterly & yearly plans

2. Amazon Prime Video

Amazon Prime Video entered India in 2016, when the OTT landscape was still developing. Early on, industry experts doubted Indian consumers' willingness to pay for subscriptions, but Amazon's major library and regional content strategy helped overcome this.

- Subscriber base: 65.9 million in India

- Content Library: 4,500+ films and 80+ TV shows in India, streaming in over 30 languages

- Global Reach of Indian Content: In 2023, Indian shows trended in Prime’s global top 10 in 43 out of 52 weeks.

- Ambitious slate: In 2023, Prime announced its largest slate yet, with 40 original series and movies in the next two years

- Revenue (global): $14 billion in 2023, a 12% year-on-year increase

3. JioCinema

JioCinema was launched by Jio Platforms in 2016, initially exclusive to Jio mobile users. Its integration into smart TVs with brands like Intex, TCL, and Xiaomi helped expand its reach, but the platform saw significant growth after the acquisition of sports streaming rights and partnerships with major studios.

- Launched JioCinema Premium in May 2023, offering ad-free access to global content for ₹29/month, making it the most affordable premium service

- Subscriber base: 15 million paying users as of 2023

- Market share: 5.91%

- Key Milestone: In April 2022, JioCinema came under Viacom18, following a major investment from Bodhi Tree Systems, focused on boosting its streaming capabilities

- Content Library: Includes HBO and NBCUniversal titles after striking deals in 2023, taking on Netflix and Disney+ Hotstar directly

- IPL Viewership: In 2023, 62 crore viewers watched the IPL on JioCinema, a 50% rise in total viewership, making it the most-watched live-stream event globally

By the way, the depth you see here is just a feeler of the depth we teach at GrowthX 💫

GrowthX is an invite-only club of over 3000 members who are product, marketing, and business leaders, and founders from top internet-first companies like Google, Canva, CRED, Stripe, Netflix, and more 💎

We teach our members how to scale revenues via frameworks that can be applied starting next Monday morning. The GrowthX Membership is built on 3 core pillars:

1. Learning experience: Where you learn the science of revenue-led growth with frameworks actionable the next Monday morning.

2. Curated community: Where you access a safe space for you to soundboard anything that is stressing you at work.

3. Career outcomes: Over 35% of members are founders & are able to hire growth teams to scale revenue for their companies while operators are able to get into breakout leadership roles.

Explore GrowthX Membership 🏆

Market Share

How does Netflix make money?

Netflix's money comes mostly from subscriptions—people like us paying a monthly fee to watch shows and movies. That's the main way they make money. But there are a couple of other ways too. Here’s a breakdown 👇

- Subscriptions: This is Netflix’s bread and butter. Millions of people across the world pay monthly or yearly fees to access Netflix’s massive library of shows, movies, and documentaries. The more subscribers they have, the more money they make.

- Content Licensing: Sometimes, Netflix licenses (or rents) its own shows to other platforms, like TV channels or airlines. They charge these companies to use Netflix content for a certain amount of time.

- Original Content: Netflix also makes money by producing its own content (like Stranger Things, The Crown, etc.). Some of these Netflix Originals become super popular globally, which not only attracts new subscribers but also brings in revenue if Netflix licenses them out to other services.

Cost Levers

Running Netflix isn’t cheap—it costs billions! Here are the major areas where Netflix spends money, known as cost levers:

1. Content Creation and Acquisition

👉🏻 Making their own shows and movies is one of Netflix's biggest expenses.

These projects require huge budgets, star actors, expensive locations, and special effects. Think about how much a show like The Witcher must cost with all that medieval fantasy stuff—it adds up fast!

But creating original content is how Netflix stands out. People subscribe just to watch these exclusive shows.

👉🏻 Apart from their Originals, Netflix also pays other studios for popular shows and movies to keep their library fresh.

Shows like Friends or Breaking Bad used to be on Netflix, but Netflix had to pay for the rights to stream them. The more popular the content, the more expensive the licensing fee.

2. Technology and Infrastructure:

👉🏻 Netflix isn’t just about creating content—it’s about delivering that content smoothly to millions of users across the world at the same time. To do this, they rely on massive cloud services like AWS (Amazon Web Services) to store all the shows and movies and stream them in high quality.

This comes at a huge cost since maintaining servers and ensuring fast, buffer-free streaming for everyone is expensive.

👉🏻 Behind the scenes, Netflix has a tech team constantly improving the platform—whether it’s making sure the app works well on your phone, TV, or tablet, or refining their algorithms so you get perfect show recommendations.

This ongoing research and development also costs a lot.

3. Marketing and Customer Acquisition:

👉🏻 Netflix spends a ton on marketing to attract new subscribers and keep current ones hooked.

You’ve probably seen Netflix ads everywhere—on social media, billboards, or even your favourite YouTube channel.

They also run massive campaigns when big shows or movies launch, like global events or partnerships with influencers to create buzz.

4. Global Expansion:

👉🏻 As Netflix expands worldwide, it can’t just offer English-language content.

They need to dub or subtitle everything in different languages, whether it’s Hindi, Spanish, or Korean. For example, if Netflix wants to be big in India, they need shows and movies in Hindi, Tamil, and other regional languages, with accurate translations. That costs money.

👉🏻 Each country has its own regulations—some are strict about what can be shown or require Netflix to follow local tax and content rules. Adapting to these different markets means more costs.

Market Opportunity

1. Opportunity in Regional Content

India isn’t just about Hindi or English—it’s a country with tons of languages like Tamil, Telugu, Bengali, and Malayalam. A large chunk of people, especially in non-Hindi speaking areas, prefer content in their own language.

Here’s the exciting part: 54% of content produced for OTT platforms is expected to be in languages other than Hindi and English, which shows how massive this opportunity is!

To add to that, nearly 80% of OTT users in India come from Tier 2 and Tier 3 cities and rural areas, where regional content is even more popular.

Regional platforms like Aha, Hoichoi, and STAGE have seen success by focusing on specific languages and dialects. For example, Aha (which focuses on Telugu) already has 2.5 million paid subscribers, and STAGE (focusing on Haryanvi and Rajasthani) has 2,75,000 paid subscribers.

If Netflix dives deeper into regional languages, they could stand out from competitors like Amazon Prime and Disney+ Hotstar, who are still very Hindi and English focused.

2. Penetrating Tier-2 and Tier-3 Cities

Netflix is still seen as a platform for people in bigger cities, but the real future growth lies in Tier-2 and Tier-3 cities.

With 918 million internet users in India and around 375 million of them coming from rural areas, there’s a vast audience Netflix hasn’t fully tapped yet.

These are smaller cities where internet usage is booming, and people are craving affordable entertainment. With smartphone penetration expected to reach over 90% of total mobile subscribers by 2028.

One way to grab their attention is by offering lower-cost subscription plans or mobile-only options, just like they’ve done before. This approach can attract more users from these smaller cities, especially since there’s a growing demand for content but people aren’t looking to spend big money on subscriptions.

3. New Pricing Model:

Here’s something really interesting: Netflix could change its pricing model to better match how Indians consume content.

Right now, Netflix uses a typical Subscription Video on Demand (SVoD) model, where people pay a monthly fee. The cheapest plan is ₹149 per month, which is for mobile/tablet use only. But here’s the catch—many Indian users aren’t platform-loyal. They don’t care if it’s Netflix or Prime Video; they just want to watch the specific content they love.

So, how about offering a different pricing model?

Instead of asking users to commit to a whole month of Netflix, Netflix could introduce a pay-per-use system, something like ₹48 for 48 hours of access to content. This would let users pay for the time they want to spend watching, instead of paying for a month they might not fully use.

Plus, it could work like this: the 48 hours of watch-time must be used within 7 days, and users would have to watch a few ads along the way (kind of like YouTube but with premium content).

The depth you see here is just a feeler of the depth we teach at GrowthX 💫

GrowthX is an invite-only club of over 3000 members who are product, marketing, and business leaders, and founders from top internet-first companies like Google, Canva, CRED, Stripe, Netflix, and more 💎

We teach our members how to scale revenues via frameworks that can be applied starting next Monday morning. The GrowthX Membership is built on 3 core pillars:

1. Learning experience: Where you learn the science of revenue-led growth with frameworks actionable the next Monday morning.

2. Curated community: Where you access a safe space for you to soundboard anything that is stressing you at work.

3. Career outcomes: Over 35% of members are founders & are able to hire growth teams to scale revenue for their companies while operators are able to get into breakout leadership roles.

Explore GrowthX Membership 🏆

Challenges

1. Price Competition

Here’s the thing—Netflix is great, but it’s expensive compared to JioCinema.

The cheapest Netflix plan in India is ₹149 per month, but it’s limited to mobile devices. In contrast, JioCinema offers a monthly plan for just ₹29, which can even go up to ₹59. That’s still incredibly cheap!

Even JioCinema's annual plan is a steal at ₹299 or ₹599 per year, which is way less than what Netflix charges for just one month on its top tier. Let’s break it down even more: JioCinema’s ₹29 plan costs just ₹0.97 per day, while Netflix’s mobile plan comes out to ₹4.97 per day.

This is a huge price difference, and for users in Tier 2 and Tier 3 cities, or rural areas, price really matters. Almost 80% of OTT users in India are from these regions, so JioCinema’s super-low prices might be way more attractive to them than Netflix’s higher costs.

2. Dialects and Local Content

India is a land of diverse languages and dialects, and this is where platforms like STAGE are making waves.

STAGE is basically trying to become the “Netflix for Bharat” by offering content in local dialects like Haryanvi and Rajasthani. STAGE started in 2019, and even though it’s pretty new, it’s already grabbed 275,000 paid subscribers.

That’s impressive, especially considering it’s focused on regional, non-Hindi content. Other platforms like Aha (with 2.5 million paid subscribers) and Hoichoi (focused on Bengali content) are also doing well.

Here’s why this is a challenge for Netflix: 54% of content on OTT platforms is now in languages other than Hindi and English. People want to watch shows and movies in their own language, and regional platforms are filling that need.

Netflix, on the other hand, still focuses heavily on Hindi and English content. If it doesn’t ramp up its regional-language game, Netflix could miss out on this massive audience that wants localized content in their own dialects.

3. Password Sharing and Subscription Fatigue

Password sharing has been a long-standing issue for Netflix, and it’s really starting to hurt their bottom line. In India, password sharing is super common—families and friends often share one account across multiple households.

But Netflix is trying to crack down on this. They’ve already announced that people will start getting emails if they’re sharing passwords outside their households. While this move is designed to stop revenue loss, it’s a tough one for Netflix because users might get annoyed or just cancel their subscriptions.

There’s also the risk of subscription fatigue—people are tired of paying for so many different platforms.

In India, there are already 57 OTT platforms competing for attention. If users feel overwhelmed by all the subscriptions, they might just opt for cheaper platforms or stick to free content with ads. This puts pressure on Netflix to not only fight password sharing but also keep people from canceling their subscriptions altogether.

By the way, we have much more value in store for you 💫

FREE in-depth play books on some of the core problems you might be struggling with at work.

These are not hacks but deep-actionable frameworks built by the Learning & Experience team at GrowthX.

You can access foundations on 👇

5. SEO

6. Monetisation